•

•

Web Development for Financial Brands: Why Industry Knowledge Matters

This article is for informational purposes only and does not constitute legal advice. Brokers should consult qualified legal and compliance professionals for jurisdiction-specific guidance.

Key Takeaways

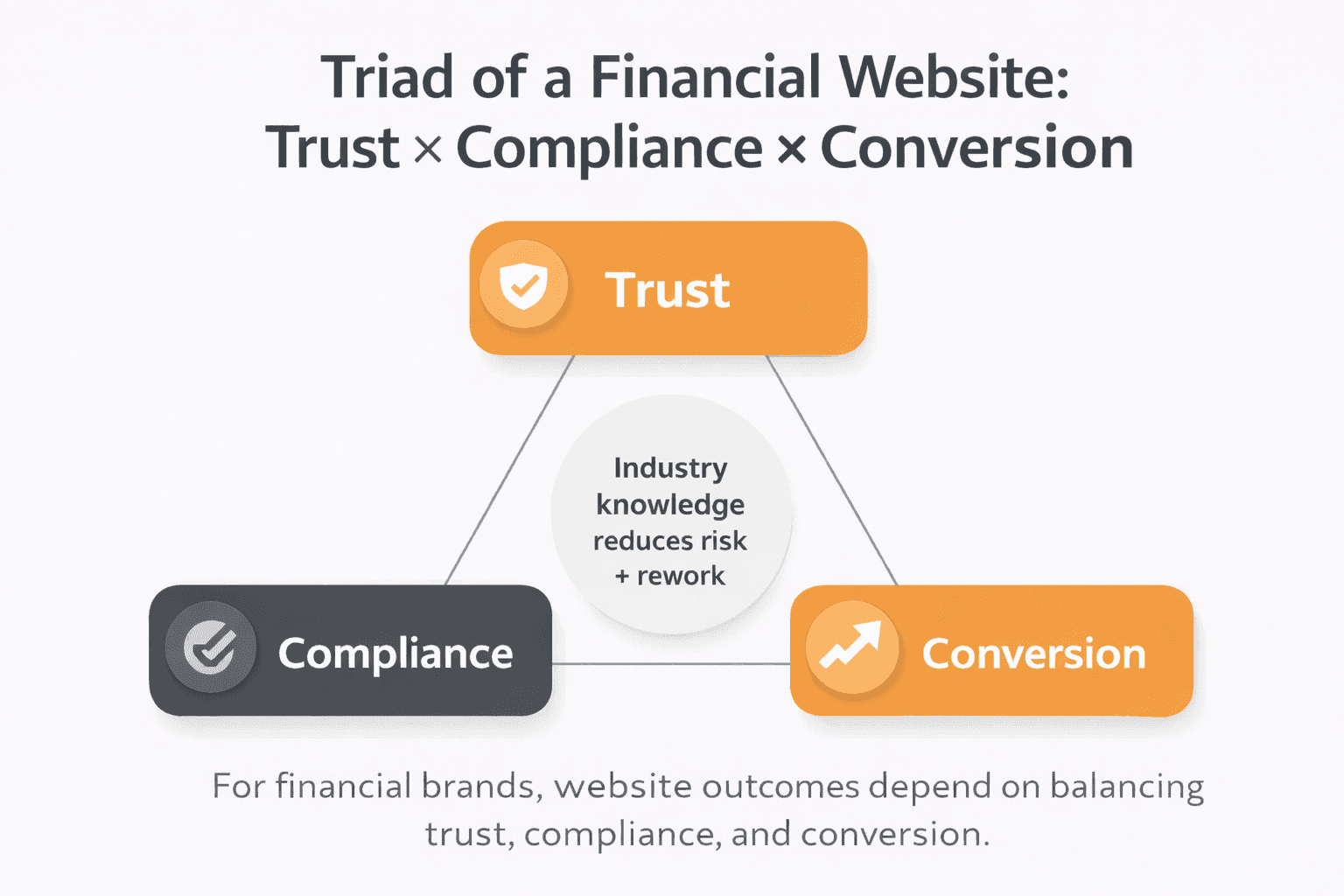

Financial websites are compliance surfaces, trust gates, and conversion engines — not just marketing pages.

Industry knowledge prevents late-stage rework by anticipating disclosures, data-handling requirements, and stakeholder approval cycles before the build begins.

Trust-building UX in finance is about clarity, proof, and safety signals — not creative flair.

Small mistakes in tracking, disclosure placement, or form handling carry outsized risk in regulated environments.

The best outcomes come from aligning marketing, product, compliance, and security from day one — not as a final checklist.

What Makes Web Development for Financial Brands Different From “Normal” Web Projects?

Finance websites operate under higher trust, security, and regulatory expectations — so small mistakes become business risks.

Every website is expected to look credible. In financial services, that bar is significantly higher, and the consequences of missing it aren’t just aesthetic — they’re commercial and regulatory.

A prospective customer landing on a lending platform, neobank, or brokerage website is making a rapid risk assessment. They’re asking: Is this real? Is it safe? Is it regulated? What are the actual terms? They’re doing this in seconds, often on mobile, before they’ve read a single content block. At the same time, a regulator — or a potential institutional partner — may be assessing the same site with more scrutiny and more time.

What makes financial services web development genuinely different:

Higher scrutiny from more audiences. Customers, investors, partners, regulators — and even competitors — judge the site. A compliance officer at a prospective partner company may review your disclosures before they look at your pitch deck.

Sensitive data flows. Contact forms, demo requests, and onboarding flows can touch personally identifiable information (PII). How that data is collected, stored, and transmitted matters — legally and operationally.

More governance layers. Legal and compliance review cycles, version control of policy pages, and stakeholder sign-offs aren’t exceptions — they’re standard in regulated environments.

Products that require precision. Fees, risk levels, eligibility criteria, jurisdictional restrictions, and regulatory status aren’t “just copy.” They’re disclosure obligations that should be structured into the site’s architecture from the beginning.

A generalist agency can build a beautiful site. What they often can’t do is anticipate these constraints before a legal review sends the project back to square one — three weeks before launch.

Where Industry Knowledge Changes Outcomes in a Financial Website Build

Industry knowledge shows up in the decisions that prevent rework: scope, architecture, content claims, disclosures, tracking, and QA.

The most expensive problems in financial web projects don’t come from bad design. They come from decisions made early — or skipped entirely — that only surface when compliance, legal, or a senior stakeholder reviews the site for the first time.

Here’s where industry knowledge makes the difference:

Discovery questions that go beyond “what pages do you need?” An experienced fintech web development team asks: Which jurisdictions are you operating in? Are you regulated, registered, or exempt? Who are you targeting — retail, professional, institutional? Do you have existing legal or compliance documents that need to live on-site? Is there anything your team cannot say publicly?

Page architecture built for trust, not just navigation. A homepage that buries licensing information three scrolls down fails both UX and governance expectations. Information architecture should reflect what users and reviewers need to find — not just what converts.

Content that doesn’t create compliance liability. Vague claims like “best returns” or “guaranteed income” are obvious red flags. Subtler risks — implied performance promises, jurisdiction-inappropriate product descriptions, and unclear fee structures — are less visible but just as costly.

Tracking built around consent, not assumed by default. Privacy-safe measurement requires intentional setup, not a cookie banner added at the last minute.

Launch readiness that includes evidence, not just aesthetics. Security hardening, QA documentation, accessibility checks, and content approval trails are deliverables — not optional extras.

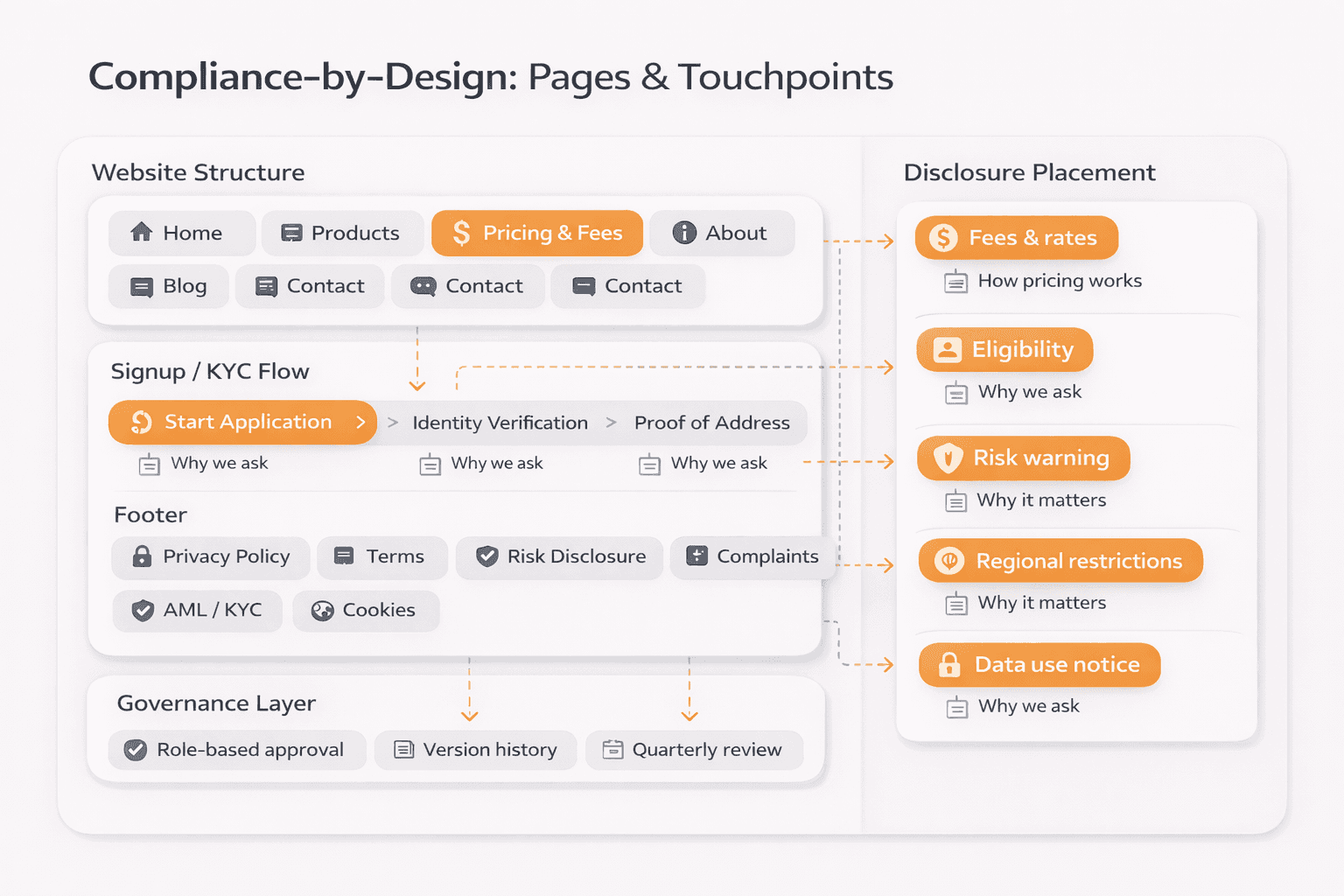

What “Compliance-by-Design” Looks Like on Financial Brand Websites

Compliance-by-design means building disclosure and policy requirements into the site structure and workflows — not bolting them on at the end.

The most common (and costly) pattern in financial website development looks like this: the agency finishes the design, the client submits it for legal review, and the legal team sends back a list of changes — some structural, some content-based, some requiring entirely new pages. The timeline slips. The budget grows. Everyone gets frustrated.

This happens because disclosures weren’t part of the brief.

Common compliance content surfaces that should be planned from the start (not an exhaustive legal list — requirements vary significantly by product and jurisdiction):

Content surface | Purpose |

|---|---|

Risk warnings | Required for investment, trading, and lending products in many regulated jurisdictions |

Product / service disclosures | Fees, terms, eligibility, and what the product does and doesn’t do |

Licensing / registration information | Confirmation of regulatory status and relevant body |

Privacy policy | Data-handling obligations under GDPR and equivalent frameworks |

Terms and conditions | Legal relationship between the business and the user |

Complaints handling | Required in many jurisdictions; must be easy to find and clear |

Regional access restrictions | Geo-fencing notices, jurisdictional eligibility statements |

AML policy page | Increasingly expected, especially for crypto and payments businesses |

Regulators such as ASIC have published guidance (e.g., Information Sheet 291) indicating that website disclosures — including Financial Services Guide obligations — should be accessible, legible, and accurate. Other regulators (including the FCA, SEC, FINRA, and CySEC) hold similar expectations, expressed through different rules and guidance.

Why templates fail: A generic “risk warning” copied from another site may not reflect your product, your jurisdiction, or your customer type. Disclosures are business-specific. What you disclose — and where — should be reviewed and approved by qualified legal counsel, not assembled from boilerplate.

Post-launch governance matters too. Compliance isn’t a launch event. Requirements change. Products evolve. A compliant website needs a defined process for updating policies, version-controlling changes, and documenting approvals.

📋 Pre-Launch Governance Checklist

All policy pages reviewed and approved by legal/compliance

Version history documented

Risk warnings verified against applicable regulatory guidance

Content-approval workflow established for future updates

Disclosure placement confirmed in the context of the user journey (not just as a footer link)

Why Trust UX Is Different in Finance

Finance UX must reduce perceived risk quickly through clarity, transparency, and proof — because the user’s downside feels immediate.

When someone considers opening a trading account, applying for a loan, or transferring money to a new platform, they’re not just evaluating the product — they’re evaluating whether they’ll regret the decision. That changes how UX needs to work.

Web design for financial services is not primarily about aesthetics. It’s about answering three questions in the first few seconds:

What is this? (Product clarity)

Is it safe? (Trust and legitimacy signals)

What’s the catch? (Fees, risks, eligibility transparency)

Trust signals that move the needle in regulated markets include:

Regulatory status, licence numbers, and licensing body logos (verified and current)

Security posture indicators (SSL, data-handling statements, relevant certifications)

Named leadership, physical presence, and institutional partners

Clear fee structures — not hidden in footnotes

Social proof calibrated to the audience (institutional logos often carry more weight than star ratings for B2B fintech)

High-friction flows — account opening, KYC onboarding, and funding — deserve particular attention. KYC onboarding is often where conversion breaks down. Users encounter unexpected document requests, unclear error messages, or a flow that feels insecure. An experienced team designs for the friction, not around it — explaining what’s needed and why, setting expectations for timing, and building recovery paths for common failure states.

Accessibility isn’t optional. WCAG guidelines exist for good reason — and in financial services, they matter even more because products serve broad demographics. Poor accessibility excludes users, increases legal exposure, and often correlates with weak overall UX. It should be a QA requirement, not an afterthought.

Security and Privacy Basics That Generalist Teams Often Miss

A financial brand website should treat security and privacy as default requirements — especially around forms, tracking, and integrations.

Most marketing websites don’t handle truly sensitive data. Financial services websites often do — or are perceived to — which means the security bar is higher and the trust cost of getting it wrong is steep.

Areas where financial services website security gaps most commonly appear:

Form hygiene. Contact forms, demo request forms, and account inquiry forms on fintech sites often collect names, emails, company names, and sometimes more. Data minimisation is the right default — collect only what you need, handle it correctly, and don’t pipe it through tools that aren’t appropriately secured or governed.

Spam and bot prevention. Low-effort protection on financial forms creates both operational noise and reputational risk.

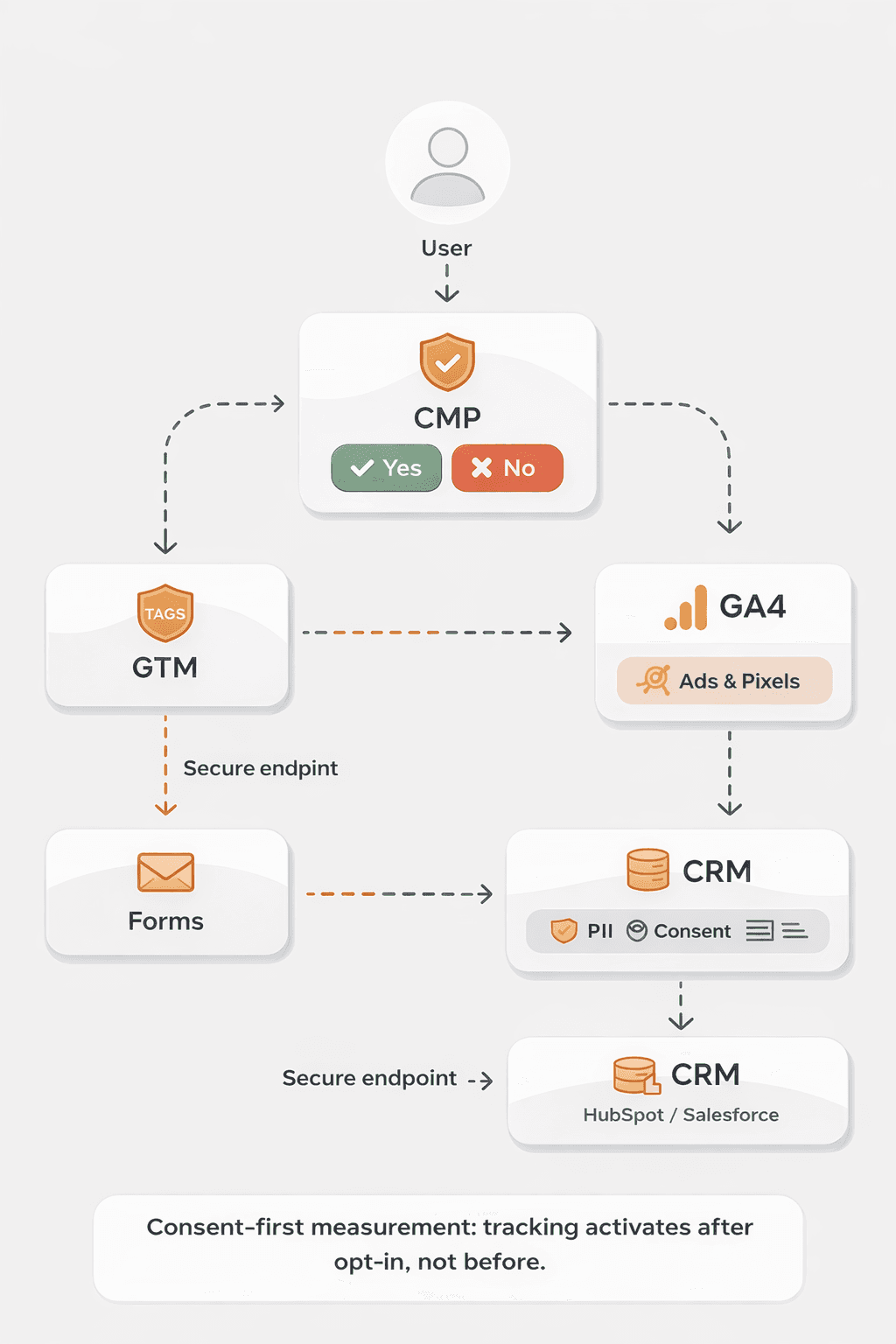

Cookie consent done properly. A cookie banner that loads tracking scripts before consent is granted is, in many cases, non-compliant under GDPR/ePrivacy frameworks — it’s “cookie-banner theatre”. Proper consent implementation typically means non-essential tracking is blocked by default and only activated after explicit opt-in. Consent management platforms (CMPs) — including providers in the OneTrust category — can support this when configured correctly.

Analytics consent configuration. GA4 consent mode, as documented by Google, allows measurement to continue in a privacy-preserving way when users decline tracking — but it must be set up intentionally, not assumed.

OWASP fundamentals. The OWASP Top 10 provides a widely referenced baseline for web application security. Relevant controls — input validation, secure headers, dependency management — apply to financial brand websites as well as full applications.

PCI DSS requirements apply where payment card data is handled directly. In most marketing-site scenarios, the right approach is to avoid touching card data entirely by routing payments through compliant processors — but this should be explicitly scoped, not assumed.

Platform and Stack Choices for Financial Brands

The right platform depends on whether you’re building a marketing site, a secure client portal, or both — and on your governance needs.

Platform choices in financial website development carry operational implications that go beyond developer preference.

Marketing sites (Webflow, Framer, and similar). For marketing-focused financial brand websites, modern no-code/low-code platforms offer genuine advantages: speed to build and iterate, strong CMS capabilities, performance optimisation out of the box, and controlled publishing workflows that reduce the risk of unauthorised changes going live. These work well for fintech startups, growth-stage brands, and teams without in-house developer capacity.

Custom engineering (React/Next.js and similar). When the website needs to authenticate users, integrate with internal systems, surface account data, or support complex onboarding flows, a custom-built approach — often React or Next.js — offers the flexibility and control that marketing platforms can’t match. The trade-off is cost, maintenance overhead, and the need for ongoing technical resource.

Multi-jurisdiction and multi-language considerations. If your brand operates across regulatory boundaries, the platform should support jurisdiction-specific content, regional access restrictions, and potentially different disclosure sets by market.

Governance fit. Who updates content after launch? Who approves changes? What’s the release process? The right platform for a financial brand is one the actual team can use safely — not just the agency that built it.

Common Mistakes When Generalist Agencies Build Financial Websites

🚩 Generalist Red Flags to Watch For

Missing or incorrectly placed risk disclosures — discovered during legal review, post-design

Performance or return claims in copy that haven’t been reviewed by compliance/legal

Contact and inquiry forms collecting sensitive data without proper handling protocols

Cookie banners that load tracking scripts before user consent is captured

“Beautiful” page designs that don’t answer the trust questions users are actually asking

No documentation, approval trail, or governance process for post-launch updates

Accessibility skipped or deferred (“we can do that later”)

Platform choices made for agency convenience, not the client’s operational needs

A Practical Checklist: How to Scope a Financial Website Project Correctly

If you can define these inputs early, your build will be faster, safer, and cheaper.

Before finalising the brief, confirm:

Products and services — exactly what you’re offering, and what you’re not

Jurisdictions and audiences — where you operate, who you can target, and any restrictions

Required disclosures and policies — what’s needed, and who approves them internally

Trust proof inventory — licences, audits, certifications, key partnerships, security posture

Conversion goals — demo request, application start, account opening, partner inquiry, or a combination

Integrations — CRM, email platform, scheduling tool, analytics, consent/CMP, and any bespoke systems

Content ownership — who writes, who approves, and what the review cycle looks like

QA requirements — security baseline, performance targets, accessibility standard, browser/device coverage

Post-launch governance — update process, version control, and an ongoing compliance review cadence

💡 Industry Knowledge Checklist

An experienced financial web partner will raise most of these in the first discovery session — unprompted. If they don’t, it’s worth noting.

How to Choose a Web Development Partner for a Financial Brand

The best partner can explain your risks and constraints before you do — and has a clear process for compliance, security, and approvals.

When evaluating a fintech web development agency or studio, the right questions go beyond portfolio and price.

Ask about process:

How do you handle legal/compliance review cycles during the project?

Who is responsible for structuring disclosure pages — your team or ours?

How do you configure analytics and cookie consent for regulated clients?

What does your QA process cover, and how is it documented?

Look at the portfolio:

Does it include work for regulated financial brands — not just “fintech-adjacent” companies?

Do the sites communicate trust, risk, and clarity — or are they primarily visual showcases?

Is there evidence of post-launch governance or ongoing client relationships?

Watch for red flags:

Any guarantee of compliance — no agency can guarantee regulatory compliance; that’s a legal and business responsibility

No stakeholder or approvals plan — a red flag in regulated environments where multiple sign-offs are normal

Vague answers about data handling, form security, or analytics consent

No mention of governance, versioning, or post-launch update processes

Next Steps: Why Fintech-Specialised Teams Deliver Better Outcomes

Getting a financial brand website right — on time, on budget, and without late-stage compliance rework — requires a team that understands the environment before the brief is written.

WSA works with fintech startups, financial service providers, and regulated brands on websites built to perform in high-trust, high-scrutiny environments. That means industry-aware discovery and scoping, trust-first information architecture, compliance-ready content structure developed in close coordination with your legal and compliance team, and rigorous launch discipline across QA, performance, analytics, and maintainability.

You can see the approach in practice across the WSA project portfolio.

Ready to Build a Financial Website That Works for Your Business — Not Against It?

Talk to a team that understands the environment before the brief is written. Industry-aware scoping. Trust-first UX. Compliance-ready structure. Launch discipline.

FAQ

Do financial services websites need special compliance pages?

Most do — but the specific requirements vary significantly by product type, business model, and jurisdiction. A retail investment platform operating under FCA oversight has different disclosure obligations than a B2B payments API provider. The right approach is to define your regulatory perimeter early, work with qualified legal or compliance counsel to confirm what’s required, and build those content surfaces into the site’s information architecture from the start — not as a late-stage addition. The cost of getting this wrong isn’t just legal; it’s the rework cycle when a compliance review rejects a design that was never structured correctly in the first place.

What are the biggest risks of hiring a generalist web agency for a financial brand?

The most common risks are late-stage rework when legal or compliance reviews flag missing disclosures or risky claims; privacy and tracking mistakes from cookie consent setups that don’t meet GDPR or equivalent standards; form and data-handling gaps that create security exposure; and design-first delivery that prioritises aesthetics over the trust clarity and information hierarchy financial audiences actually need. In aggregate, these risks translate to delayed launches, unplanned budget, and websites that underperform against conversion and trust goals.

How should financial brands approach analytics and cookie consent?

The governing principle is consent-first: non-essential tracking — including standard analytics — should be blocked by default and activated only after a user explicitly opts in. A cookie banner that loads tracking scripts before consent is captured is unlikely to meet the requirements of most European (and equivalent) privacy frameworks, regardless of how it looks. GA4 consent mode provides a mechanism for privacy-preserving measurement when users decline, but it must be configured intentionally. A consent management platform (CMP) is typically the right infrastructure layer, paired with an analytics setup that’s tested against your consent configuration — not assumed to be working correctly.

What platform is best for a financial brand website?

It depends primarily on what the site needs to do. For marketing-focused financial brand websites — product pages, content, lead generation, partner pages — modern platforms like Webflow can offer strong governance controls, CMS flexibility, and fast iteration cycles that suit regulated environments. For anything involving authenticated users, account data, or complex integrations, a custom engineering approach (e.g., React/Next.js) provides the control needed. The secondary consideration is operational fit: who maintains the site post-launch, what the update and approval process looks like, and whether the platform can support multi-jurisdiction content if needed.

How long does a financial brand website project usually take?

For a well-scoped marketing site, four to ten weeks is a reasonable range, depending on complexity, content readiness, and integration requirements. More complex builds — including portals, authenticated experiences, or multi-jurisdiction implementations — take longer. The variable most often underestimated by financial brands is the compliance review cycle. Legal and compliance approvals aren’t a final step; they’re a recurring process throughout the project. Building review windows into the timeline from the outset — rather than scheduling them as a single gate before launch — is one of the clearest signs of a team that understands how financial website development actually works.

Whether you’re launching something new or improving an existing platform, we’re ready to discuss your goals and explore the best way forward.