•

•

SCB Bahamas Broker Licence Documents: A Practical Checklist & How to Display Information on My Website

This article is for informational purposes only and does not constitute legal advice. Brokers should consult qualified legal and compliance professionals for jurisdiction-specific guidance.

You are three months into your SCB Bahamas licence application. Your legal team has assembled the corporate filings, your compliance officer has drafted the AML policy, and your business plan is ready for review by the Securities Commission of The Bahamas.

Then a banking partner asks to see your website.

Half the SCB Bahamas licence documents you prepared for the application also need to be publicly accessible on your broker site. Risk disclosures, client agreements, AML policies — they are not just filing requirements. They are pages your clients, regulators, and institutional partners expect to find the moment they visit your domain.

This article gives you a practical forex broker document checklist — what the SCB requires, where each document belongs on your website, and the mistakes that cost brokers their standing.

Key Takeaways

The SCB requires corporate, compliance, and client-facing documents — each with specific publication rules on your broker website

AML/KYC policies, risk disclosures, and client agreements must be publicly accessible — not buried in PDFs or collapsible footers

Document placement directly affects regulatory audits, banking partner due diligence, and client trust

A structured legal footer, dedicated legal hub, and compliant onboarding flow are structural requirements — not design extras

Keeping documents versioned and current prevents the most common audit failure: outdated policies on live pages

The SCB Document Checklist Every Broker Needs

SCB Bahamas licence documents fall into three categories: corporate and incorporation records, compliance and AML/CFT policies, and client-facing legal agreements. All three must be submitted as part of the SCB licence application under the Securities Industry Act, 2024 (which replaced the 2011 Act). Many of them also carry ongoing publication obligations once your brokerage goes live.

Here is the complete forex broker document checklist, broken down by category.

Required Corporate and Incorporation Documents

Corporate documents establish your brokerage as a legal entity in The Bahamas. These are foundational Bahamas broker licence requirements — without them, the SCB will not begin reviewing your application.

Certificate of Incorporation — issued by the Registrar General of The Bahamas

Memorandum and Articles of Association — defining the company's purpose, share structure, and governance rules

Register of Directors and Officers — full names, nationalities, and contact details

Shareholder register and beneficial ownership disclosure — identifying all persons with significant control

Business plan — covering operational model, target markets, technology stack, revenue projections, and risk management approach

Proof of registered office address in The Bahamas

Proof of capital adequacy — bank statements or audited financials demonstrating minimum capital (USD 120,000 for dealing as agent only; USD 300,000 for dealing as agent and principal)

Required Compliance and AML/CFT Documents

Compliance documents prove your brokerage can prevent financial crime and meet SCB regulatory standards. The Bahamas aligns its AML framework with FATF recommendations and OECD Common Reporting Standards — so these documents must reflect international standards, not just local requirements. Additional obligations may also apply under the Financial and Corporate Service Providers Act, 2020.

AML/CFT policy manual — covering client due diligence, transaction monitoring, suspicious activity reporting to the Financial Intelligence Unit (FIU), and record-keeping procedures

KYC procedures documentation — specifying identity verification methods, enhanced due diligence triggers, and politically exposed persons (PEP) screening

Compliance officer appointment letter — the SCB requires a designated compliance officer physically present in The Bahamas

CEO appointment and fit-and-proper documentation — CVs, professional references, police clearance certificates, and evidence of relevant industry experience for all directors and key personnel

Professional Indemnity Insurance — proof of coverage protecting clients against inadequate service

Internal controls and risk management framework — describing decision-making processes, organisational structure, and risk mitigation procedures

IT security policy — covering data protection, trading platform security, and disaster recovery

Client-Facing Legal Documents

Client-facing documents govern the relationship between your brokerage and its traders. These are the broker compliance documents that must be accessible on your website — not just filed with the SCB.

Terms and Conditions (Client Agreement) — the full contractual framework between your brokerage and clients

Privacy Policy — covering data collection, storage, processing, GDPR compliance (if serving EU clients), and data subject rights

Risk Disclosure Statement — clearly outlining the risks of trading CFDs, forex, and other leveraged products

Order Execution Policy — describing how trades are executed, potential conflicts of interest, and execution venues

Complaints Handling Procedure — detailing how clients can file complaints and the resolution process

Fee Schedule / Cost Disclosure — transparent listing of spreads, commissions, swap rates, and any non-trading fees

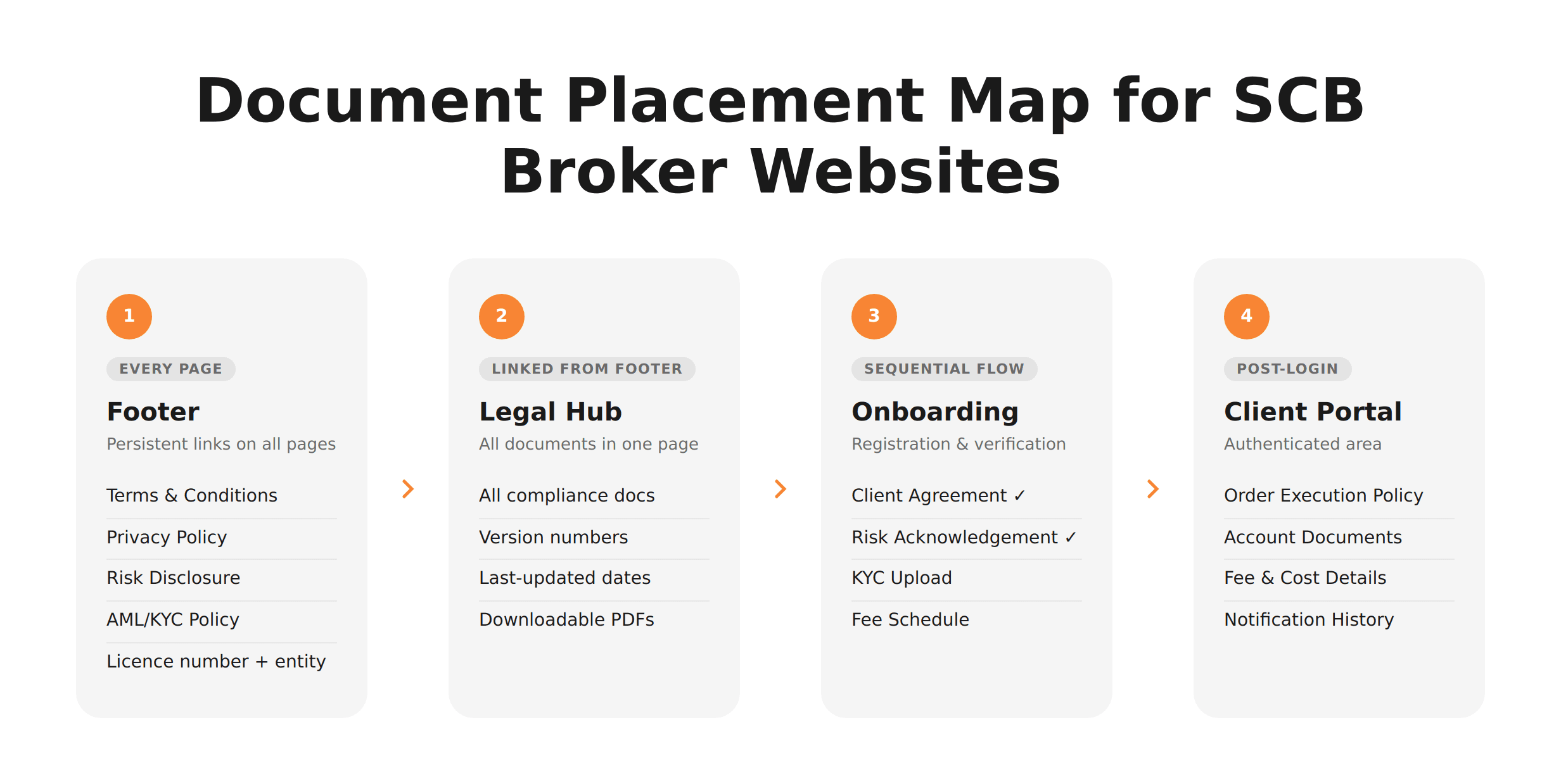

Where to Publish Each Document on Your Broker Website

Publishing broker compliance documents correctly on your website is not optional. Regulators, banking partners, and liquidity providers all review your site during due diligence. A missing document or a broken link to your AML policy can delay a banking relationship by weeks.

Here is the document placement map for SCB-regulated brokers.

Legal Footer and Dedicated Legal Hub

Your broker website legal footer is the single most reviewed element during compliance checks. Every page on your site should include footer links to:

Terms and Conditions

Privacy Policy

Risk Disclosure Statement

AML/KYC Policy (summary or full)

Regulatory information — licence number, entity name, SCB registration status

Best practice: Create a dedicated /legal hub page that lists all compliance documents in one place, with clear titles, last-updated dates, and downloadable PDF versions where appropriate. This page should be linked from the footer and from your main navigation.

Brokers WSA works with typically structure the legal footer as a persistent, non-collapsible section visible on every page — not hidden behind a "click to expand" toggle.

Client Portal and Onboarding Documents

Some documents belong behind the login wall — specifically those tied to the client relationship:

Client Agreement (full) — presented during registration, requiring explicit acceptance before account creation

Order Execution Policy — accessible within the client dashboard

Fee Schedule — linked from account type pages and visible within the trading portal

KYC document upload instructions — integrated into the verification flow

Building a forex broker website that converts starts with compliance-aware UX. KYC compliance on your broker website depends on clear instructions at each verification step. Traders should know exactly what documents they need to upload, in what format, and why.

Risk Disclaimers — Placement and Visibility Rules

Risk disclaimers for brokers require specific placement:

Homepage — a persistent risk warning banner or footer line citing the risks of CFD/forex trading

Account opening pages — risk disclosure before the registration form, not after

Marketing and promotional pages — every page mentioning trading conditions, spreads, or potential returns must include a visible risk statement

Footer — a concise risk warning on every page, linking to the full Risk Disclosure Statement

The SCB expects risk disclosure to be prominent and accessible — not a footnote in 10px grey text.

Need Your Broker Website Structured for SCB Compliance?

WSA builds broker sites with legal pages, footer architecture, and onboarding flows designed around regulatory requirements — not added after launch.

Document Versioning and Update Workflow

Outdated compliance documents on a live broker website are one of the most common audit failures. An AML policy drafted in 2023 sitting on a site in 2026 signals either negligence or non-compliance — neither is acceptable to the SCB or your banking partners.

How to Keep Legal Pages Current Without Downtime

Set a document review cycle. Every compliance document should be reviewed at least annually, or immediately when the SCB issues new guidance or when your business model changes (new products, new jurisdictions, new payment methods).

Use version numbering. Each published document should include a version number and "last updated" date visible on the page. Example: AML/CFT Policy v3.2 — Last updated: January 2026.

CMS-based workflow. If your site runs on Framer or Webflow, use a structured CMS approach: draft the updated document, stage it for review, and publish the new version while archiving the previous one. This prevents downtime — the old version stays live until the new one is approved and deployed.

Notify existing clients. When material terms change (Privacy Policy, Client Agreement), send an email notification and add a banner to the client portal announcing the update.

Mistakes That Cost Brokers Their SCB Standing

The most expensive compliance mistakes are not missing documents — they are documents that exist but are buried, outdated, or incomplete.

Missing or Buried Documents on Public Pages

A broker launches with a clean, visually polished site. The marketing team optimises for conversion — but the legal footer links to a generic "Legal" page with placeholder text. During a banking partner review, the compliance team cannot find the AML policy. The banking relationship stalls for 6 weeks.

This happens more often than it should. A comprehensive broker website compliance checklist can help you catch these issues before a partner review does. Common failures:

AML policy exists as an internal PDF but is not linked anywhere on the public site

Risk disclosure is present but buried three clicks deep, behind a collapsible section

Licence number and entity name are inconsistent between the homepage and the legal pages

Privacy Policy covers GDPR but omits Bahamas-specific data processing details

AML Policy Gaps That Auditors Flag

The AML/CFT policy is the single most scrutinised document in any SCB audit. Common gaps:

No SAR (Suspicious Activity Reporting) procedure — the policy mentions monitoring but does not describe how reports are filed with the FIU

Missing PEP screening process — no documented procedure for identifying and handling politically exposed persons

Outdated thresholds — transaction monitoring thresholds that do not reflect current FATF guidance

No training schedule — no evidence that staff receive regular AML training

Each of these gaps can trigger a formal SCB inquiry. In serious cases, the Commission has the authority to impose administrative penalties or revoke a licence entirely.

Is Your Broker Website Audit-Ready?

From legal footer structure to AML page placement — WSA builds broker websites that pass compliance reviews the first time.

Building a Compliance-Ready Broker Site With WSA

WSA Design builds broker websites with compliance architecture integrated from the first wireframe. For brokerages operating under Bahamas broker licence requirements — or any other jurisdiction — the legal page structure, footer links, and onboarding flows are scoped during discovery, not patched in before launch.

What this means in practice:

Legal hub and footer are part of the initial site map — not added after the marketing pages are done

Document placement follows regulatory mapping — each jurisdiction's requirements are reflected in the page architecture

CMS structure supports versioning — legal pages are managed through a structured content model that supports version history and approval workflows

Onboarding flows include compliance checkpoints — KYC document upload, risk acknowledgement, and client agreement acceptance are built into the registration path

If you are preparing for an SCB licence and building your broker website in parallel — whether you create a broker website from scratch or redesign an existing one — the document checklist above is where to start. The website architecture should reflect it from day one.

FAQ

What documents does the SCB Bahamas require for a broker licence?

The SCB requires three categories of documents: corporate records (Certificate of Incorporation, Articles of Association, shareholder register, business plan, proof of capital), compliance documents (AML/CFT policy, KYC procedures, compliance officer appointment, Professional Indemnity Insurance, IT security policy), and client-facing legal agreements (Terms and Conditions, Privacy Policy, Risk Disclosure, Order Execution Policy). The full list depends on the licence type — dealing as agent only versus dealing as agent and principal. Consult the SCB's official guidance or a qualified licensing advisor for your specific situation.

Where should AML and KYC policies be published on a broker website?

Your AML/KYC policy should be accessible from two locations: the website footer (linked on every page) and a dedicated legal hub page that centralises all compliance documents. The policy should be available as both a web page and a downloadable PDF. Banking partners, liquidity providers, and regulators expect to find it within one click from any page on the site.

How often should broker compliance documents be updated?

At minimum, every compliance document should be reviewed annually. Documents must also be updated immediately when the SCB issues new regulatory guidance, when your business model changes (new products, jurisdictions, or payment methods), or when FATF issues revised recommendations. Each update should include a visible version number and "last updated" date on the published page.

What is the minimum capital requirement for an SCB Bahamas broker licence?

The minimum capital requirement depends on the licence type. For dealing as agent only (STP/A-book model), the minimum is USD 120,000. For dealing as agent and principal (market maker/B-book model), the minimum is USD 300,000. Proof of capital must be provided through bank statements or audited financial statements submitted to the SCB.

Can the SCB revoke a licence for missing website documents?

The SCB has the authority to investigate licensed firms, issue directives, impose administrative penalties, and revoke licences for serious compliance breaches. While a single missing document may not immediately trigger revocation, persistent non-compliance with publication obligations — especially missing AML policies or risk disclosures — can lead to formal enforcement action. Banking partners and liquidity providers may also terminate relationships independently if they identify compliance gaps on your website during their own due diligence reviews.

Ready to Build Your SCB-Compliant Broker Website?

WSA structures legal pages, document placement, and onboarding flows for regulated brokers — so your site is audit-ready before you launch.

Conclusion

The SCB Bahamas licence documents you prepare for your application are also the foundation of your broker website's compliance architecture. Corporate filings stay in the regulator's files — but AML policies, risk disclosures, client agreements, and regulatory information must be visible to every visitor, banking partner, and auditor who lands on your site.

Getting the documents right is half the work. Placing them correctly — in the footer, the legal hub, the onboarding flow, and the client portal — is what separates a compliant broker website from one that stalls partnerships and triggers regulatory inquiries.

WSA Design builds broker websites with this compliance structure built in from the start. If you are preparing for an SCB licence and need a site that passes due diligence on day one, the next step is a conversation.

Whether you’re launching something new or improving an existing platform, we’re ready to discuss your goals and explore the best way forward.