•

•

Fintech Conversion Optimization: CRO Framework for Financial Brands

Most conversion rate optimization advice was written for e-commerce or SaaS. Swap a headline, test a button color, shorten a form—done.

That playbook breaks down in fintech. You can’t remove a required disclosure. You can’t freely rewrite a fee claim without compliance sign-off. You can’t streamline KYC by cutting corners. And a “signup” is rarely the metric that drives revenue—verification, funding, and first transaction do.

Fintech conversion optimization is the discipline of increasing the number of users who complete compliant, high-value actions—verified signups, funded accounts, first transactions—without inflating fraud risk, compliance exposure, or customer acquisition cost. It requires a system, not a list of tips.

This article gives growth, product, and marketing teams at fintech companies—as well as digital leaders at established financial brands—a repeatable CRO framework for financial brands that maps to how regulated funnels actually work. Whether you’re fighting KYC drop-off, watching paid acquisition efficiency stall, or preparing to scale your first growth program, the same structured approach applies.

Key Takeaways

Fintech CRO is won in onboarding and trust—not button-color tests or headline swaps.

Measure activation and quality (verified, funded, first transaction), not vanity signup counts.

Most fintech conversion loss is either friction (hard to complete) or anxiety (feels risky)—and the fix is different for each.

Compliance and risk belong inside the CRO program, not at the end of it.

A disciplined framework with consistent experimentation outperforms sporadic redesigns every time.

Quick wins (copy clarity, tech fixes, trust signals) can appear in weeks. Sustained gains come from a 90-day+ program cadence.

What Is Fintech Conversion Optimization?

Fintech conversion optimization is the systematic practice of increasing the percentage of users who complete compliant, high-value actions—like verified signup, account funding, and first transaction—without increasing fraud, regulatory risk, or customer acquisition cost.

This definition matters because it repositions the goal. In e-commerce, “conversion” typically means a completed purchase. In conversion rate optimization for fintech, the equivalent endpoint is usually multi-step: a user must sign up, pass identity verification, connect a payment method or deposit funds, and then complete a meaningful first action—a trade, a payment, a loan drawdown, a card spend.

Where fintech funnels typically break

Landing page clarity: Vague value propositions, compliance-hedged language that says nothing, or mismatch to the traffic source

Onboarding friction: Too many fields, poor mobile UX, unclear requirements, slow load times

KYC anxiety: Users abandoning at document upload or identity verification because it feels invasive, scammy, or confusing

Funding and authentication steps: SCA/3DS friction, unclear fee structures, or bank-linking failures

No clear next action: Verification passes, but users don’t know what to do next—so they do nothing

Optimizing any one of these in isolation produces marginal results. Addressing them as a connected system—with measurement at every step—is what moves the business.

What Makes CRO Harder in Regulated Financial Brands

Financial CRO has unique constraints—compliance review cycles, restricted claims, and higher user anxiety—so any framework must be designed for trust and governance from the start.

This is the part that catches fintech teams off guard when they try to apply standard financial services conversion optimization methods borrowed from SaaS or retail.

Compliance constraints on copy and offers. Claims about rates, returns, savings, or fees are regulated. Changing a headline or CTA can require legal or compliance review. That slows testing velocity and makes “rapid iteration” harder than it sounds.

Fraud and risk guardrails are non-negotiable. You can’t optimize by weakening identity verification or reducing friction in ways that increase fraud exposure. Any experiment that touches verification flows must be cleared against defined risk thresholds.

Unavoidable steps in the funnel. KYC/KYB, AML checks, SCA/3DS authentication, and PCI DSS–compliant payment flows exist because regulations require them. The goal isn’t to remove these steps—it’s to reduce the perceived cost of completing them.

Longer conversion cycles and attribution complexity. In lending or wealth management, users may take days or weeks to move from first click to funded account. Last-click attribution masks the true conversion story, and lifecycle touchpoints (email, SMS, in-app nudges) often make or break activation.

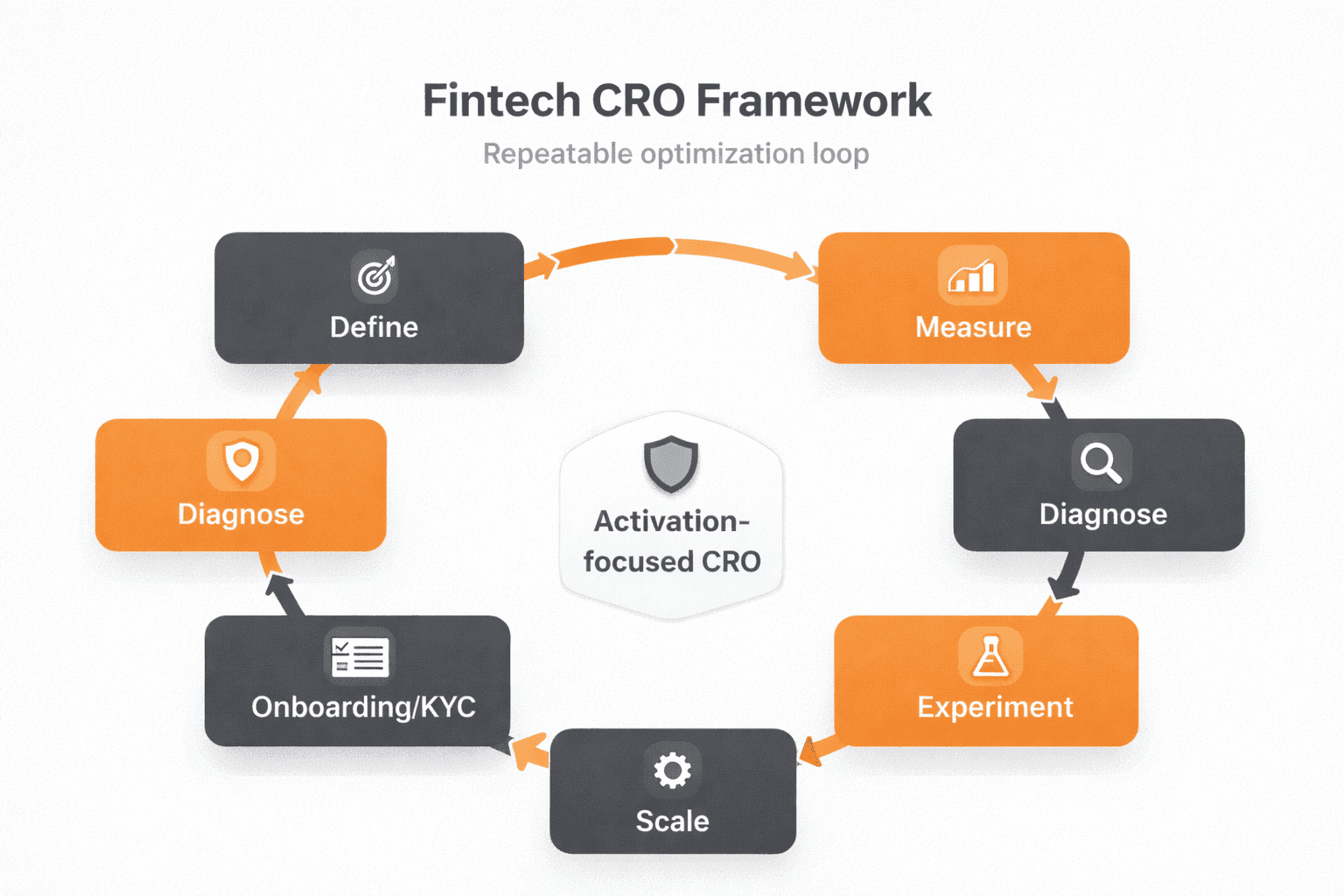

The CRO Framework for Financial Brands

A fintech CRO framework is a repeatable loop: define success → measure the funnel → diagnose friction and anxiety → build trust → optimize onboarding and KYC → run compliant experiments → scale what works.

Rather than running isolated tests, high-performing fintech teams run this loop continuously. Each cycle produces cleaner data, stronger hypotheses, and a documented library of what works—so the program compounds over time.

Step | Phase | Key Output |

|---|---|---|

1 | Define success metrics | North star KPI + guardrail metrics |

2 | Instrument the funnel | Event map, baseline dashboard |

3 | Diagnose friction vs. anxiety | Prioritized drop-off audit |

4 | Build trust into the flow | Trust-signal map + testable hypotheses |

5 | Optimize onboarding and KYC | Reduced drop-off (without weakening controls) |

6 | Run compliant experiments | Prioritized backlog + validated learnings |

7 | Operationalize and scale | Design system updates, activation playbooks |

Each step is covered in detail below.

Visual reference 1: A loop diagram illustrating the seven-step CRO cycle—Define → Measure → Diagnose → Trust → Onboarding/KYC → Experiment → Scale—with arrows connecting each phase, emphasizing repeatability.

Not sure which option fits your business?

From startup brokerages to established platforms, WSA delivers websites that convert traders, satisfy regulators, and scale across markets.

Step 1: Define Conversion the Fintech Way

In fintech, the “real” conversion is activation—a user who’s verified and has completed a first-value action—not a form fill or email capture.

Optimizing for signup volume is one of the most common—and most damaging—mistakes in fintech growth. It inflates acquisition metrics while hiding the real problem: most signups never become funded, transacting customers.

Activation milestones by product type

Payments: First successful payment or wallet top-up

Neobanking: Verified account + first deposit + card activation

Lending: Completed application + approval + first disbursement

Trading/wealth/crypto: Verified + funded + first trade or investment

B2B fintech: Qualified demo + completed KYB + first transaction volume

Each of these represents a first-value moment—the point where the user experiences the core product promise. That’s the conversion event to optimize toward.

Guardrail metrics: what you must not worsen

Alongside conversion KPIs, define the conversion rate optimization metrics fintech teams must protect:

Fraud rate and chargeback rate

KYC fail rate and manual review rate

Support ticket volume per activation step

Complaint rate and regulatory escalation rate

These guardrails ensure conversion gains are real—not artifacts of loosening controls that create downstream costs.

Step 2: Fix Measurement Before You Fix UX

If you can’t see where users drop off, you can’t optimize—fintech CRO starts with clean event tracking and reliable funnel visibility.

This is the step most teams skip or underinvest in, which is why their experiments produce inconclusive results. A GA4 funnel tracking fintech setup—or an equivalent product analytics stack—must be in place before meaningful testing begins.

Minimum event map

Every fintech funnel should instrument, at minimum:

Landing page view

CTA click (primary CTA)

Signup start

Signup complete

KYC start

KYC submit

Verification pass / fail (with failure reason)

Funding start

Funding success

First-value action (first trade, payment, deposit, etc.)

Recommended tooling

Web analytics: GA4 + Google Tag Manager for page-level and marketing attribution data

Product analytics: Mixpanel or Amplitude for event-level funnel analysis and cohort tracking

Data routing: Segment to normalize events across tools and teams

Session replay: FullStory, Hotjar, or Contentsquare for qualitative investigation of drop-off points

Server-side tracking: In regulated environments where client-side scripts create consent or data-residency issues, server-side tracking (e.g., GTM server-side or a CDP) can deliver cleaner, consent-mode-compatible data

Practical implementation notes

Use consistent event naming across web and app. Resolve cross-device identity where possible (especially in mobile-first funnels). QA tracking before any experiment launches—bad data is worse than no data. This is a core component of any honest fintech CRO audit checklist.

Visual reference 2: A funnel visualization showing conversion rates at each step of a representative fintech onboarding flow—from landing page view to first transaction—with step-level drop-off percentages and annotations highlighting the highest-loss transitions.

Ready to Build a Fintech Website That Actually Converts?

Stop guessing where your funnel is leaking—start with a structured diagnostic.

Step 3: Diagnose Conversion Loss Using Friction vs. Anxiety

Most fintech drop-off comes from either friction (too hard to complete) or anxiety (feels too risky)—and the fix for each is different.

Misdiagnosing the cause leads to wasted experiments. A progress bar won’t solve KYC abandonment driven by low trust. More trust badges won’t help if users keep failing document upload because guidance is unclear.

Friction indicators

High error rates on form fields

Long time-to-complete on individual steps

Repeated failed attempts at document upload or bank linking

Slow page or app performance (especially on mobile)

Unclear field requirements (format errors, missing instructions)

Anxiety indicators

Long dwell time on specific steps with no forward progress (hesitation more than confusion)

Exits at the point of personal data entry or bank connection

Support messages expressing fear of scams or data misuse

User-testing participants saying, “I’m not sure I trust this”

Methods to use

Funnel and time-to-complete analysis in Mixpanel/Amplitude: segment by device, region, channel, and cohort

Form analytics: field-level drop-off data from tools like FullStory or Hotjar to locate input friction

Session recordings: watch real users navigate high-drop-off steps—you’ll spot issues no quantitative tool surfaces

Support ticket mining: tag inbound tickets by funnel stage; volume by stage is a proxy for confusion and anxiety

Moderated user testing: ask directly—“What would stop you from continuing here?”—using scripts that probe friction vs anxiety in conversion without leading participants

Step 4: Build Trust Signals Into Every Conversion Step

Trust signals are conversion elements in fintech—users need proof of legitimacy before they’ll share identity data or move money.

The challenge is that many fintech teams treat trust signals as design decoration rather than structured, testable conversion assets. Trust signals for fintech should be mapped to specific funnel steps and tested with the same rigor as any other hypothesis.

What to test and where

Above the fold (landing page):

Clear statement of who the product is for and what it does

Regulatory status or licensing information (e.g., FCA-authorised, SEC-registered)—where applicable and verifiable

Partner or integration logos (Visa, Mastercard, established bank partners)

Press mentions and review counts (accurate and current)

During onboarding:

Inline explanations for why each data point is requested

Clear statements on how data is stored and used

Time estimates for completion

Progress indicators showing how far users are in the process

Around pricing and fees:

Transparent fee tables or calculators before the point of commitment

“No hidden fees” claims only where they can be substantiated to compliance standards

Clear explanation of what happens after signup

Security and compliance signals:

Encryption and data-security statements in plain language

PCI DSS compliance, SOC 2 certification, or equivalents where applicable

Fraud-protection explanations that reduce uncertainty

Reducing ambiguity—especially around what happens next—is one of the highest-leverage trust interventions in fintech. Financial brand credibility design isn’t about looking impressive; it’s about making users feel informed and safe enough to proceed.

Step 5: Optimize Onboarding and KYC Without Weakening Controls

The goal isn’t less KYC—it’s a smoother, clearer, more forgiving KYC journey that keeps good users moving while maintaining risk standards.

Fintech onboarding optimization and KYC conversion optimization are the highest-leverage areas in most fintech funnels—and the most misunderstood. Teams either accept KYC drop-off as inevitable or try to remove steps (creating compliance and fraud risk). The real opportunity is improving the experience around required steps.

Practical approaches to reduce onboarding drop-off in fintech

Progressive disclosure: Collect data only when it’s needed, not all upfront. Asking for proof of address before a user has any reason to trust you is a common anxiety trigger.

Risk-based routing: Where compliance and risk teams permit, route lower-risk applicants through lighter initial flows and request additional verification only when required (a risk-based onboarding approach).

UX clarity around document requirements: Show examples of acceptable documents. Explain image-quality requirements before capture attempts, not after failures. Use real-time validation to catch issues before submission.

Drop-off recovery: If a user abandons mid-verification, trigger a resume flow via email or SMS with a direct deep link back to the exact step. Add in-app nudges and support access at the moment of failure.

Reduce rework: Pre-fill known information across steps. Don’t ask for data the user has already provided. Inconsistent personal information across a multi-step form is a common source of KYC failure.

Explain the regulatory “why”: Framing requests as compliance requirements (“We’re required by law to verify your identity—this takes about 3 minutes”) reduces anxiety compared to unexplained asks.

Step 6: Create an Experimentation Backlog That Compliance Can Approve

Regulated CRO scales when you build a testing pipeline compliance can review quickly—using pre-approved templates, documented guardrails, and component libraries.

This is where compliant experimentation becomes a program-design issue, not just a testing issue. The bottleneck in most financial brands isn’t ideas—it’s the review cycle. The solution is to standardize how experiments are documented, categorized, and approved.

Hypothesis template

Each experiment in the backlog should include:

Problem: What drop-off or friction point does this address?

Insight: What data or research supports the hypothesis?

Change: What will be different in the variant?

Expected impact: Which metric should move, and by roughly how much?

Segments: Which user groups does this apply to?

Guardrails: Which guardrail metrics will be monitored? What triggers a pause?

Compliance review needed? Yes/No—with notes on what specifically requires sign-off

Prioritization model

Score each hypothesis on expected impact, confidence in the insight, and implementation effort—then apply a compliance-risk modifier. High-risk tests need more review time and should be prioritized only when expected gains justify the overhead.

Test types that work well in fintech

Messaging clarity tests on landing pages (audience match, value-prop clarity, social proof placement)

Step sequencing tests in onboarding (what to ask and when)

Error handling and guidance improvements around KYC and payment steps

Fee transparency modules (how and when fees are surfaced)

Proof and credibility blocks (security statements, partner logos, review counts)

Performance optimizations (page load, mobile rendering)—speed is a direct conversion lever and one of the safest test categories from a compliance perspective

Tools like Optimizely, VWO, or Convert handle web-level experimentation. LaunchDarkly is well suited for server-side or feature-flag-based testing in regulated environments where client-side testing creates compliance exposure.

Step 7: Focus on Activation, Not Just Acquisition

The highest ROI in fintech CRO often comes from improving post-signup activation—turning verified users into funded, transacting customers.

Traffic and signups get attention. Activation is where revenue lives. A user who signs up and never funds an account costs you acquisition spend with zero return. The fintech activation rate—the percentage of signups who reach first value—is often the most important (and least-optimized) metric in the funnel.

How to improve activation through the onboarding funnel in fintech

First-value milestone design: Make the first meaningful action obvious, achievable quickly, and rewarding. For a trading app, this might mean completing a first simulated trade or setting up a watchlist before requiring funding.

In-product guidance: Tooltips, onboarding checklists, and contextual education reduce drop-off in products with a learning curve (investing, lending, business accounts).

Lifecycle messaging tied to drop-off triggers: If a user completes KYC but doesn’t fund within 24 hours, trigger a specific message—not a generic “welcome back.” Segment by drop-off point and personalize by intent.

Personalization by intent: Users who arrive saying “I want to invest for retirement” need different onboarding emphasis than users who arrive saying “I want to trade crypto.” Segment flows where possible.

Reduce time-to-value: Use guided setup flows, progress checklists, and smart defaults to get users to their first meaningful action as fast as product and compliance constraints allow.

Visual reference 3: A side-by-side comparison table showing a standard linear onboarding flow versus a progressive-disclosure onboarding flow, with annotations highlighting where anxiety-reducing copy, trust signals, and step-level recovery mechanisms are inserted in the optimized version.

Common Mistakes in Fintech CRO

Even well-resourced teams repeat these errors. Avoiding them is part of what makes fintech conversion optimization a discipline rather than a one-off project.

Optimizing for signup volume instead of verified, activated quality. Raw signup rates are a vanity metric if they don’t translate to funded accounts.

Shipping changes without measurement. No event tracking, no baseline, no way to know what helped or hurt.

Treating compliance as a final “sign-off” step. Involving compliance only at the end slows everything. Build review into planning.

Hiding fees or key requirements until late steps. Users who feel misled don’t just abandon—they leave complaints, bad reviews, and churn.

Overloading onboarding with unnecessary questions upfront. Collect the minimum required information first; add context-appropriate questions later.

Ignoring failure states. KYC fails, bank-link fails, and payment-auth fails are high-volume drop-off events that often receive little optimization attention.

Running random A/B tests instead of a prioritized backlog tied to identified funnel leaks and a clear hypothesis framework.

CRO Program Checklist for Financial Brands

Use this as a fintech CRO audit checklist to assess readiness or identify gaps before a new initiative begins.

North star metric and guardrail metrics defined and agreed across growth, product, risk, and compliance

Funnel event tracking implemented, QA’d, and verified against real user sessions

Top drop-off steps identified and segmented by device, channel, and region

Friction vs. anxiety diagnosis completed for each high-loss step

Trust signals mapped to specific funnel steps (not applied generically)

Experiment backlog built and scored using impact × confidence × effort, with a risk modifier

Compliance review workflow documented: who approves what, at which stage, within what SLA

Testing cadence established (bi-weekly or monthly sprint cycles)

Winning variants rolled into the design system and documented

Learnings archived to prevent re-testing already-answered questions

FAQ

What is the best CRO framework for fintech companies?

The most effective CRO framework for financial brands is a repeatable seven-step loop: define activation-based success metrics and compliance guardrails → instrument the funnel for step-level visibility → diagnose whether drop-off is driven by friction or anxiety → design trust interventions → optimize onboarding and KYC UX → execute compliant experiments → operationalize winners into the design system. The differentiator from e-commerce or SaaS frameworks is that compliance and risk review are built into the process, not added at the end—so the program can run continuously without stalling.

What metrics should fintech teams optimize first?

Start with activation milestones, not signup volume. A practical priority sequence is: (1) verified account completion rate, (2) funding rate among verified users, (3) first-transaction rate among funded users. These map to the actual revenue pathway. In parallel, establish guardrails—fraud rate, KYC fail rate, chargeback rate, manual review rate—so you know whether gains are real or coming at a downstream cost. Conversion rate optimization metrics fintech teams should focus on are those tied to the first-value action for your product (first deposit, first trade, first payment, first approved loan).

How do you improve KYC conversion rates without increasing risk?

KYC conversion optimization is about the experience around required checks, not removing them. Practical improvements include clearer document guidance before capture (not after failure), real-time validation, plain-language explanation of why data is needed, progressive disclosure (collect only what’s required at each step), resume links via email/SMS for drop-offs, and stronger failure-state handling with specific, actionable error messages. Risk-based onboarding—where lower-risk applicants move through lighter initial flows—can also reduce drop-off, but it must be designed and approved by compliance and risk.

Can you run A/B tests in regulated financial services?

Yes—but compliant experimentation requires governance. Use a hypothesis template with a compliance flag, build a pre-approved component library (copy blocks, disclosure placements, trust modules), define which test categories require sign-off (and within what timeframe), and use server-side or feature-flag-based tooling (such as LaunchDarkly) for tests that touch regulated flows. A/B testing in regulated industries is slower than in SaaS—but it becomes sustainable when the process is designed to work with compliance rather than around it.

What are the biggest trust signals that increase fintech conversion?

The five highest-impact trust signals for fintech are: (1) transparent, upfront fee and pricing information (hidden fees kill trust), (2) clear regulatory/licensing status (where applicable), (3) plain-language explanations of security and data handling—especially around identity verification and bank linking, (4) verifiable social proof (accurate review counts, real press mentions, recognizable partner logos), and (5) procedural clarity—progress indicators, time estimates, and clear next steps that reduce uncertainty in multi-step onboarding flows.

How long does fintech CRO take to show results?

Fintech conversion optimization results arrive at different speeds depending on the lever. Quick wins—fixing tracking issues, improving field guidance, adjusting trust-signal placement, improving mobile performance—can show measurable impact within 2–4 weeks. Structural improvements—onboarding redesigns, KYC UX overhauls, lifecycle messaging—typically show meaningful results within a 60–90 day program cycle. Sustained, compounding gains from a full CRO program (clean measurement + continuous experimentation + design-system updates) build over 6–12 months. Be wary of anyone promising dramatic lifts in days—that usually means measuring the wrong thing.

Should CRO focus on website landing pages or onboarding?

Both—but where you start depends on where the leak is. If paid traffic isn’t converting to signups, start with landing pages: message-to-audience match, value-prop clarity, trust signals above the fold, and performance. If signups are healthy but activation is weak, the leverage is inside the product: fintech onboarding optimization, KYC UX, funding flows, and post-signup lifecycle messaging. For most teams with stable traffic volume, onboarding and KYC are higher ROI because even a 5–10% improvement in verification completion or funding rate moves revenue directly, while landing-page gains often require proportional increases in ad spend to fully capitalize.

Whether you’re launching something new or improving an existing platform, we’re ready to discuss your goals and explore the best way forward.