•

•

Where to Store and Present Your Compliance Documents as an FSA-Licensed Seychelles Broker

This article is for informational purposes only and does not constitute legal advice. Brokers should consult qualified legal and compliance professionals for jurisdiction-specific guidance.

You received your Securities Dealer License from the FSA Seychelles. The capital is deposited, the compliance officer is appointed, and the office in Victoria is set up. Now you need a website that proves all of it.

Unlike CySEC or the FCA, the Seychelles FSA does not publish broker website URLs in its public register. Clients, liquidity providers, and payment processors cannot verify your domain through the regulator. Your website is the only place where your compliance documents, licence number, and regulatory status are visible to the outside world.

This article covers which compliance documents belong on your FSA broker website, how to structure a /legal/ hub that withstands LP due diligence, and what partners actually check in the first 60 seconds of reviewing your site.

Key Takeaways

The FSA Seychelles register lists entity names and licence numbers but does not publish website domains — your site is the primary verification channel for clients and partners

Compliance documents for an FSA broker website include risk disclosure, terms and conditions, AML/KYC policy, privacy policy, fee schedule, and complaints procedure

A dedicated /legal/ hub with clear navigation makes every document reachable within two clicks from the homepage

Liquidity providers and PSPs review broker websites during onboarding — missing or hard-to-find documents are a common reason for delays

Compliance pages should be part of site architecture from day one, not added after launch as an afterthought

Why Your Website Is the Primary Verification Channel for FSA Seychelles Brokers

The FSA Seychelles register lists licensed entities by name and licence number. It does not publish their website domains.

This creates a practical problem. When a potential client, introducing broker, or liquidity provider wants to confirm that your brokerage is licensed, they can check the FSA's Capital Markets register and find your entity name. But there is no link from that register to your website. The connection between your domain and your licence exists only on your own site.

The FSA Register Gap: Licence Numbers Without Domains

Compare this to CySEC. The Cyprus regulator publishes the regulated entity's website URL directly in its public register alongside the licence number. A client can click from the regulator's page to the broker's website in one step.

The FSA does not offer this. Its register under "Regulated Entities > Capital Markets" shows:

Entity name

Licence number (e.g., SD096, SD040)

Type of licence (Securities Dealer, Investment Advisor)

It does not show: website URL, contact email, physical office address, or the entity's trading name if different from the registered name.

The only time the FSA publicly connects a domain to a licence is in enforcement notices — when it warns the public that a specific website is not associated with a regulated entity. That is not the association you want.

What Clients, LPs, and PSPs Actually Look For

Nearly 200 firms hold FSA Seychelles Securities Dealer Licences. With no domain-level verification from the regulator, the broker's website becomes the differentiator. Clients and partners typically look for:

Licence number visible on the homepage — usually in the footer, sometimes in a header bar

Company registration details — registered name, IBC number, Seychelles registered address

A /legal/ section with clearly labelled compliance documents

Consistency — the entity name on the website matches the entity name in the FSA register

When these elements are present and well-structured, the website builds credibility. When they are missing or buried, it raises questions — regardless of whether the broker is genuinely licensed.

Compliance Documents Every FSA Seychelles Broker Should Publish

FSA Seychelles requires licensed brokers to maintain AML/CFT policies, risk management frameworks, and client-facing disclosures under the Securities Act 2007 and the AML/CFT Act 2020. The regulator does not prescribe an exact website disclosure checklist the way CySEC does (see the full compliance checklist for CySEC and FCA brokers). These recommendations reflect industry best practice and what LPs and PSPs expect to see.

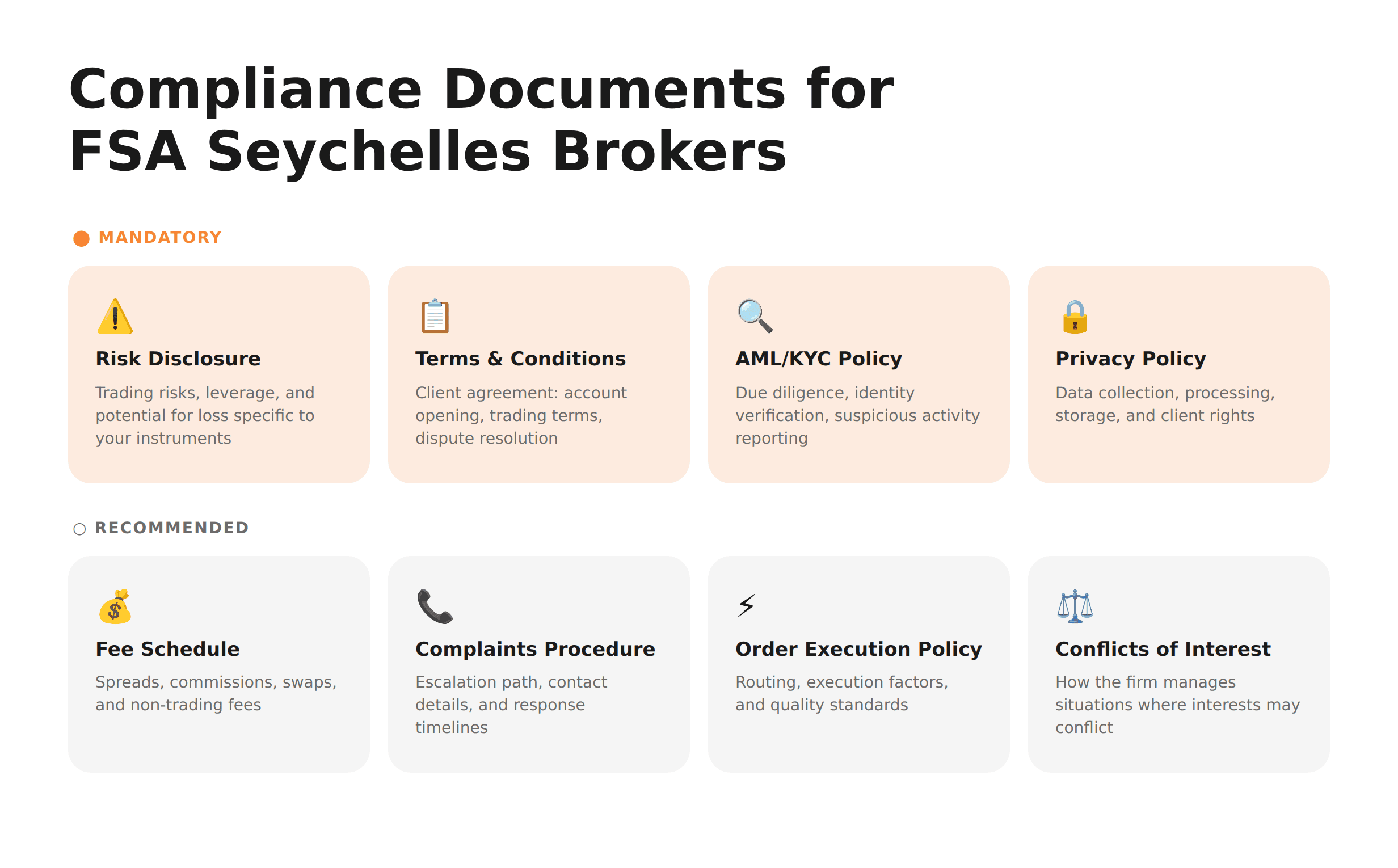

Mandatory: Risk Disclosure, Terms and Conditions, AML/KYC Policy, Privacy Policy

These four documents are non-negotiable for any FSA broker website:

Risk Disclosure — explains the risks of trading CFDs, forex, and other leveraged instruments. Should reflect the actual products and leverage offered, not generic boilerplate.

Terms and Conditions — the client agreement covering account opening, trading terms, dispute resolution, and limitation of liability.

AML/KYC Policy — outlines customer due diligence procedures, identity verification requirements, and suspicious activity reporting obligations in line with the AML/CFT Act 2020.

Privacy Policy — describes how client data is collected, processed, stored, and shared. Should reference applicable data protection standards.

Recommended: Fee Schedule, Complaints Procedure, Order Execution Policy, Conflicts of Interest

These documents are not always legally required to appear on the website, but their absence signals a gap to LP compliance teams:

Fee Schedule — transparent breakdown of spreads, commissions, swap rates, and any non-trading fees (withdrawal, inactivity)

Complaints Procedure — how clients can raise and escalate complaints, including contact details and expected response timelines

Order Execution Policy — how client orders are routed, executed, and the factors affecting execution quality

Conflicts of Interest Policy — how the broker identifies and manages situations where the firm's interests may conflict with client interests

How to Structure a /Legal/ Hub on Your Broker Website

A /legal/ hub is a dedicated section of your broker website that houses all compliance documents in one consistent, navigable location. Instead of scattering PDFs across different pages or burying links in the footer, a /legal/ hub gives every document a permanent, indexed address.

190+ Seychelles Brokers. Your Website Is How Clients Tell the Regulated Ones from the Rest

A compliance-first site structure is not optional — it is your licence made visible.

Page Hierarchy and Navigation Architecture

The structure should follow a simple parent-child model:

Homepage → /legal/ (landing page) → individual document pages

The /legal/ landing page acts as a directory. It lists every available document with a brief description and a direct link. Each document gets its own page — not a PDF download, but a full HTML page with the document content rendered in readable text.

Why HTML pages instead of PDFs? Three reasons:

Search engines index HTML content — PDFs are harder to crawl and rarely rank

Mobile readability — HTML adapts to screen size; PDFs require zoom and scroll

LP review speed — compliance reviewers can scan an HTML page in seconds; a PDF requires downloading and opening

The Two-Click Rule: Accessibility for Regulators and Partners

Any compliance document on your broker website should be reachable in two clicks from the homepage. If a compliance reviewer or LP analyst needs three or more clicks to find your risk disclosure, the structure has failed.

Click 1: Homepage → footer "Legal" link or navigation menu "Legal & Compliance" section

Click 2: /legal/ landing page → specific document (e.g., "Risk Disclosure")

This sounds simple. In practice, many broker websites bury legal documents inside accordion menus, nested dropdowns, or pages labelled with vague names like "Important Information."

Footer Links vs Dedicated Legal Section

Both approaches work — but they serve different purposes:

Footer links are the minimum. Every page on the site should include direct links to at least: Risk Disclosure, Terms & Conditions, Privacy Policy, and AML/KYC Policy.

A dedicated /legal/ section in the main navigation is the professional standard. It signals that compliance is a priority, not a checkbox. For FSA Seychelles brokers, where the website carries the full verification burden, this is the better choice.

The ideal setup uses both: a dedicated /legal/ hub accessible from the main navigation, plus footer links to the four core documents on every page.

What LPs and Payment Providers Check During Due Diligence

When a liquidity provider evaluates an FSA-licensed broker, the website review typically takes under 60 seconds. The analyst is not reading every document word by word. They are checking whether the right elements exist and are findable.

The Due Diligence Walkthrough: First 60 Seconds on Your Website

A typical LP or PSP compliance review follows this sequence:

Homepage scan (5 seconds) — licence number visible? Registered entity name present? FSA Seychelles mentioned?

Footer check (5 seconds) — links to Risk Disclosure, T&C, Privacy Policy present?

/legal/ section (15 seconds) — dedicated page exists? All core documents listed? Documents load and display correctly?

Cross-reference (15 seconds) — entity name on website matches entity name in FSA register? Licence number matches?

Risk disclosure review (20 seconds) — specific to actual instruments offered? Mentions leverage, margin, and loss potential?

If all five checks pass, the website portion of due diligence is complete. If any fail, the onboarding process stalls and the LP requests clarifications — often adding weeks to the timeline.

Red Flags That Block Onboarding

These are the most common website issues that delay or block LP and PSP onboarding for FSA Seychelles brokers:

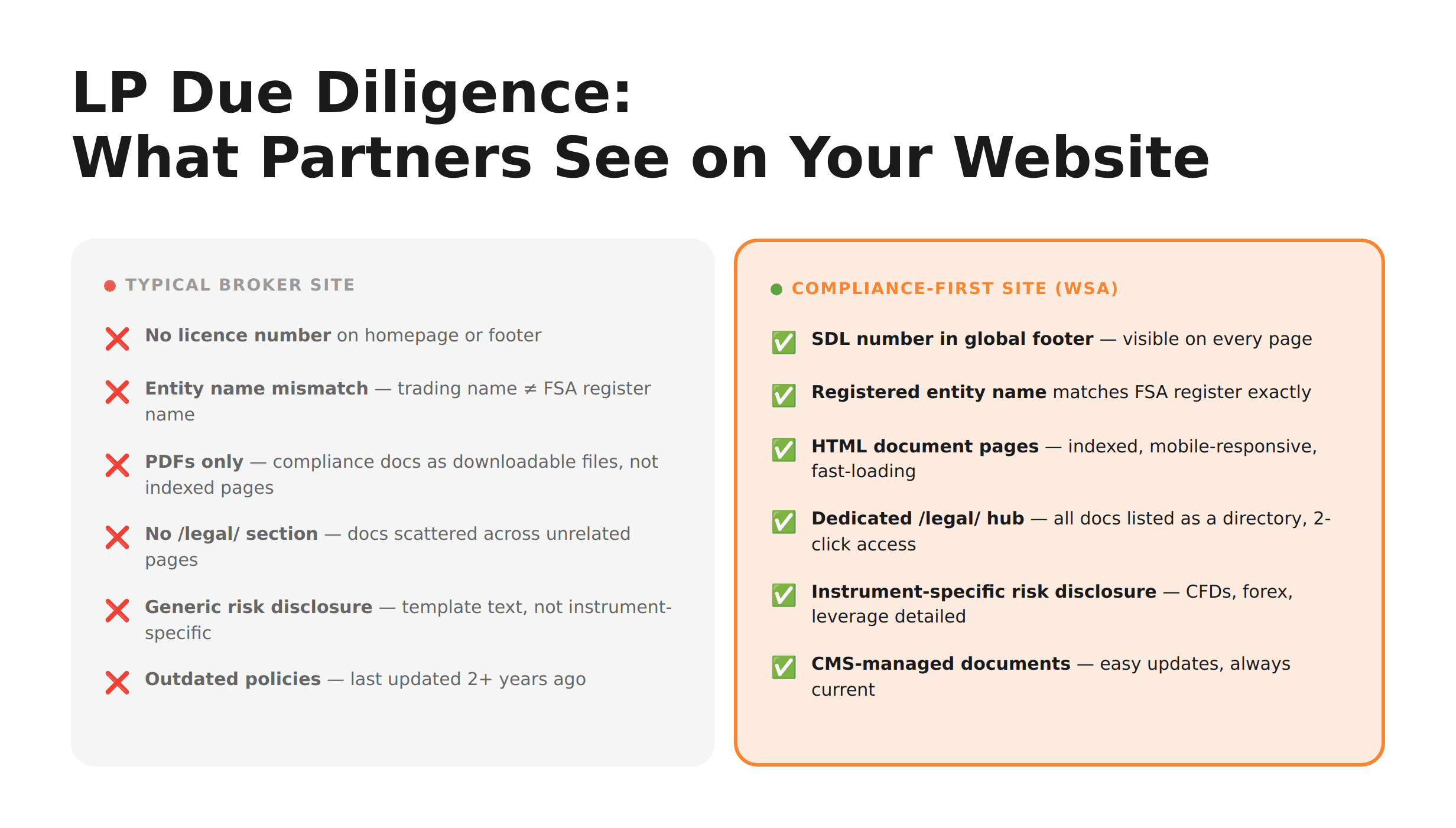

No licence number on the homepage — the simplest and most damaging omission

Entity name mismatch — trading name on website differs from registered name in FSA register, with no visible connection between them

Broken or missing document links — PDF links that return 404 errors, or pages that show empty content

Generic risk disclosure — copy-pasted from a template without adjusting for the broker's actual instruments and leverage

No /legal/ section — documents scattered across unrelated pages, or only accessible through deep navigation

Outdated documents — compliance policies that reference old legislation or show last-updated dates from two or more years ago

Building a Compliance-First Broker Website with WSA

WSA designs broker websites where the /legal/ hub is part of the information architecture from the first wireframe — not added after launch.

For Seychelles-licensed brokers, this means:

Licence and entity details in the global footer — visible on every page, matching the FSA register exactly

A /legal/ landing page with all documents listed, described, and linked

Individual HTML pages for each compliance document — indexed, mobile-responsive, and fast-loading

Risk disclosure integrated into the registration flow — not just on a standalone page, but surfaced at the point of account creation

CMS structure that makes document updates simple — when your compliance team revises the AML policy, publishing the update takes minutes, not a development ticket

This approach applies to broker websites built in Framer and Webflow (whether a new build or a broker website redesign) — both platforms support the page hierarchy, CMS integration, and footer architecture required for a compliance-first structure.

FAQ

What documents must an FSA Seychelles broker display on their website?

At a minimum, FSA-licensed brokers should publish a risk disclosure, terms and conditions, AML/KYC policy, and privacy policy on their website. Additionally, a fee schedule, complaints procedure, order execution policy, and conflicts of interest policy are recommended. The FSA does not prescribe an exact website checklist, but LPs, PSPs, and clients expect these documents to be present and accessible.

Does the Seychelles FSA require specific risk warning text on broker websites?

The FSA does not mandate a standardised risk warning format the way CySEC or the FCA does. CySEC, for example, requires brokers to display the percentage of retail accounts that lose money. The FSA's requirements are less prescriptive. However, best practice is to include a risk disclosure that specifically references the instruments you offer, the leverage available, and the possibility of losses exceeding the initial deposit. Generic or vague warnings undermine credibility with both clients and partners.

Where should compliance documents appear in broker website navigation?

Compliance documents should be reachable within two clicks from the homepage. The professional standard is a dedicated /legal/ section accessible from the main navigation or a clearly labelled footer link. The /legal/ page should serve as a directory listing all available documents. Additionally, core documents — risk disclosure, T&C, privacy policy — should have direct links in the site footer on every page.

How do liquidity providers verify an FSA Seychelles broker's licence through the website?

LPs cross-reference the entity name and licence number displayed on the broker's website with the FSA's Capital Markets register at fsaseychelles.sc. Since the FSA register does not list website domains, the LP cannot verify the connection in reverse. This means the broker's website must clearly display the registered entity name and SDL number — typically in the footer — and these must match the FSA register exactly. Any mismatch between the trading name on the site and the registered entity name creates friction.

Can I use a template site for an FSA-licensed broker, or does compliance require custom design?

When weighing a custom vs template broker website, the answer depends on compliance architecture. A template can work if it supports the required page hierarchy — a global footer with licence details, a dedicated /legal/ section, individual pages for each document, and CMS-managed content for easy updates. The problem with most templates is that they lack the information architecture for compliance pages. They are designed for marketing-first websites, not regulated broker websites. A custom or customised build, where the /legal/ hub is part of the site structure from day one, reduces the risk of compliance gaps that surface during LP onboarding.

Conclusion

Your FSA Seychelles licence proves you met the regulator's standards. Your website proves it to everyone else.

With the FSA register showing licence numbers but not domains, the burden of verification falls on the broker's own site. A well-structured /legal/ hub, consistent entity details, and accessible compliance documents are what separate a credible FSA broker website from one that raises questions during LP onboarding.

The documents are finite. The real challenge is presenting them in a way that builds trust in seconds — not minutes.

WSA builds broker websites for Seychelles-licensed firms where compliance architecture is part of the design from the first wireframe. If your site needs to pass LP due diligence before your first onboarding, that is where it starts.

Launch Your Licensed Brokerage with Confidence

We support brokers and fintechs through licensing, launch planning, and everything a regulated brand needs to go live.