•

•

Fintech CRO Agency vs In-House Team: What Works Better?

Fintech funnels aren’t like e-commerce funnels. Between identity verification, KYC/KYB checks, fraud screening, and funding steps, users face far more “forced friction” before they ever complete a meaningful action. That means improving conversion in a regulated financial product is as much about process, governance, and instrumentation as it is about button colors and headline copy.

This article is about conversion rate optimization (CRO)—not the Chief Risk Officer. In a fintech context, CRO is the structured, evidence-based practice of increasing the percentage of users who complete key actions across your funnel: starting an application, completing identity verification, making a first deposit, or placing a first transaction.

If you’re deciding whether to hire a fintech CRO agency or build an in-house team, this guide gives you a practical decision framework—not a generic pros-and-cons list. By the end, you’ll know which model fits your stage, what it costs in time and money, and why the best answer for most fintechs is a deliberate hybrid.

Key Takeaways

Most fintechs win with a hybrid model first: keep strategy, KPI ownership, and data governance in-house; outsource specialist research, experimentation support, and design execution.

If you can’t ship changes quickly, CRO won’t work—regardless of whether you hire an agency or build internally.

In fintech, compliance timelines and PII constraints often define the operating model more than budget does.

Agencies typically win on speed-to-learning and breadth of expertise; in-house teams win on product context, continuity, and institutional knowledge.

The “right” model depends on funnel volume, experimentation velocity, and proximity to product–market fit.

What Does CRO Mean in Fintech—and What Counts as a “Conversion”?

Fintech CRO is the practice of systematically improving the rate at which users progress through regulated, multi-step funnels—from first visit to verified, funded, and active.

Unlike retail or SaaS funnels, fintech conversions are layered. A single “signup” metric tells you almost nothing. The real value (and the real drop-off) lives deeper in the funnel. Common fintech conversion events to track and optimize include:

Funnel Stage | Conversion Event |

|---|---|

Awareness → Intent | Visitor → application start |

Intent → Application | Application start → application submitted |

Application → Verification | KYC/KYB submitted → KYC/KYB verified |

Verified → Funded | Verified → first deposit / funding completed |

Funded → Activated | First transaction, trade, or payment |

Retention | Second transaction; 30-day retention milestone |

One important nuance: fintech CRO optimizes for quality outcomes, not just volume. Inflating signup rates without considering fraud risk, AML exposure, or user intent isn’t a win—it’s a liability.

When Is CRO Worth Investing In for a Fintech?

CRO only performs when the fundamentals are in place. Without them, you’re paying for inconclusive data.

Before committing to an agency retainer or a hiring plan, sanity-check these prerequisites.

Green lights (CRO is worth investing in):

You have consistent traffic or activation volume (as a rough rule of thumb: 500–1,000+ monthly conversions per funnel step for statistically meaningful A/B tests)

Event tracking is reliable and covers key funnel steps (not just pageviews)

Engineering bandwidth exists—or you have feature flags—to deploy changes

There’s a defined compliance review path for UI and copy changes

Leadership agrees CRO is a priority function, not a side project

Red lights (fix these first):

Analytics instrumentation is broken or inconsistent

There’s no repeatable process for approving marketing or onboarding copy changes

Engineering can’t ship front-end changes within a reasonable sprint cycle

You have fewer than a few hundred users progressing through each funnel step per month

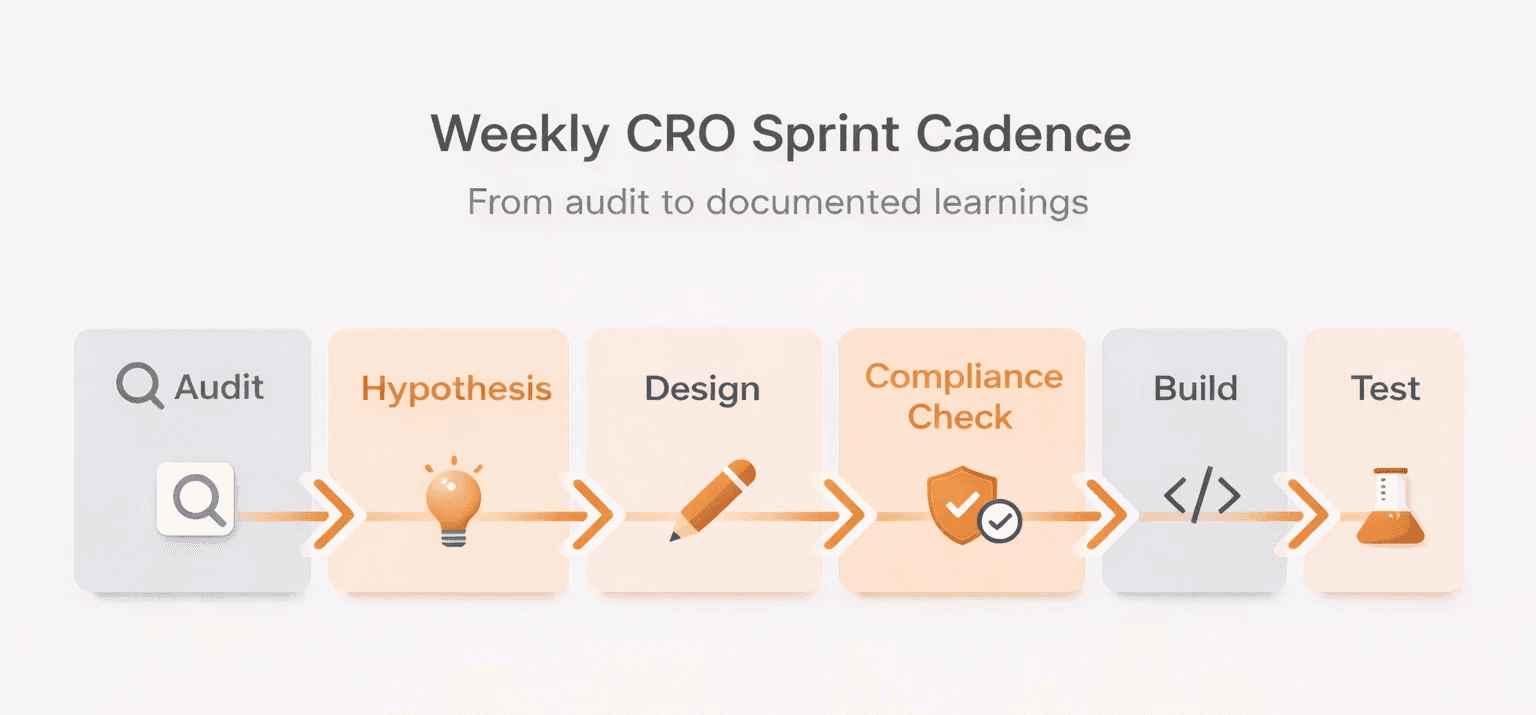

What a Fintech CRO Agency Actually Does (Week to Week)

A CRO agency runs a structured research-to-experimentation loop: auditing your funnel, building evidence-backed hypotheses, supporting test execution, and documenting learnings—not running one-off A/B tests.

A credible conversion rate optimization agency operating in a fintech context typically delivers:

Funnel and analytics audit — identifying tracking gaps, drop-off points, and instrumentation issues across GA4, Mixpanel, or Amplitude

Qualitative research — session replays and user interviews (where permitted and configured for privacy compliance), plus friction mapping across KYC and funding flows

Experiment roadmap — prioritized by expected impact, implementation effort, and compliance risk

Test design and build support — designing variants using Optimizely, VWO, or AB Tasty; or using feature-flag-based experimentation with LaunchDarkly

Onboarding and landing page UX improvements — with close attention to trust signals, error states, and form clarity

Reporting tied to business outcomes — not just conversion lift, but impact on CAC, funding rate, and activation

Fintech-specific agency work also includes navigating compliance approvals, advising on privacy-safe qualitative tooling (e.g., what Hotjar or FullStory can capture once masking and consent are in place), and avoiding dark patterns that can trigger regulatory scrutiny.

What an In-House CRO Team Looks Like (Roles, Ownership, and Dependencies)

An in-house CRO function requires more than one “growth person.” A minimum viable team covers strategy, measurement, design, and implementation—with compliance embedded as a standing stakeholder.

Here’s what a realistic in-house CRO team looks like for a growth-stage fintech:

Role | Core Responsibility | Must-Have or Nice-to-Have |

|---|---|---|

CRO Lead / Growth PM | Roadmap, prioritization, hypothesis ownership | Must-have |

Analyst | Instrumentation, funnel analysis, test measurement | Must-have |

UX Designer | Flow design, prototypes, friction audits | Must-have |

Front-End Engineer | Test builds, feature flag implementation | Must-have |

Copywriter (regulated content) | Compliant messaging for onboarding + marketing | Nice-to-have early; must-have at scale |

Compliance stakeholder | Copy/UI approval, guardrails, risk flags | Must-have (embedded, not occasional) |

A lightweight RACI for experiment governance:

Activity | CRO Lead | Analyst | Designer | Engineer | Compliance |

Hypothesis | Owns | Contributes | Contributes | — | Reviews |

Build | — | — | Owns (design) | Owns (implementation) | — |

Compliance approval | Requests | — | — | — | Owns |

Release | Coordinates | — | — | Owns | Approves |

Analysis | Reviews | Owns | — | — | — |

Cost Comparison: Agency Retainer vs Hiring a CRO Team In-House

The honest comparison isn’t just salary versus retainer—it’s time-to-learning versus long-term capability building.

In-house team (fully loaded, per year):

CRO Lead / Growth PM: $90,000–$140,000+ (market and seniority dependent)

Analyst: $70,000–$110,000

UX Designer (shared or dedicated): $75,000–$120,000

Engineering capacity (partial allocation): $60,000–$100,000+ of total compensation

Tooling: $15,000–$50,000/year (experimentation + analytics + qualitative tools)

Total conservative estimate: $250,000–$500,000+ per year before overhead, benefits, and recruiting costs

CRO agency retainer:

Typical range for a specialist fintech conversion rate optimization agency: $8,000–$25,000/month (scope dependent)

Project-based engagements (audit + roadmap): $15,000–$40,000 one-time

Annual retainer equivalent: $96,000–$300,000

The hidden cost in hiring is time. Hiring a credible in-house CRO team often takes 3–6 months, then another 3–6 months to reach steady experimentation velocity. That can mean 6–12 months without compounding learnings—while CAC keeps rising.

Speed and Experimentation Velocity: Which Model Ships Faster?

Agencies can start producing insights within weeks; in-house teams usually take months to reach a reliable experimentation cadence. But in fintech, the real bottleneck is often internal—not who runs CRO.

What typically blocks experimentation velocity in financial products:

Engineering queues — tests compete with roadmap work

QA and release cycles — regulated products often have longer validation gates

Legal and compliance review — changes touching claims, rates, fees, or regulated terms can take days to weeks to approve

Data governance — adding new tracking events may require security review before deployment

A strong CRO agency can accelerate work on marketing landing pages and top-of-funnel flows quickly. But in-app onboarding improvements—inside KYC flows, account setup, or funding screens—still depend on your internal release process. No agency can bypass your engineering queue.

The takeaway: before choosing a model, map your internal bottlenecks. If compliance and engineering cycles are the constraint, improve those first.

Not sure which option fits your business?

From startup brokerages to established platforms, WSA delivers websites that convert traders, satisfy regulators, and scale across markets.

Fintech-Specific Constraints That Change the Answer

Fintech CRO runs inside tighter constraints than most industries—and any team that ignores them will either slow down or create risk.

Key constraints to factor into your operating model:

Regulated copy and claims — interest rates, returns, fee disclosures, and KYC requirements can’t be tested freely. Claim libraries and pre-approval workflows matter.

PII and privacy constraints — session replay and behavioral tooling is often restricted on authenticated or onboarding screens, and may require heavy masking, consent, sampling, and security review.

Fraud and abuse risk — optimizing for raw conversion volume without monitoring fraud patterns can increase exposure. CRO in lending, crypto, or payments needs a risk lens.

Third-party script security — injecting experimentation scripts into authenticated environments typically requires a vendor and security review. SOC 2 and internal access policies often apply.

Accessibility and trust expectations — financial products face higher standards for accessibility and transparent UX. “Conversion tricks” that work in e-commerce can be inappropriate—or non-compliant—in fintech.

These constraints affect both models. But an experienced CRO for fintech agency will usually have workflows for them already—whereas an in-house team often has to build that muscle from scratch.

Tooling and Data: Who Should Own the CRO Stack?

Fintechs should keep data governance and instrumentation ownership in-house—even when outsourcing execution. Tooling should be chosen for the long term, not the current vendor relationship.

A practical fintech-friendly CRO tool stack:

Analytics: GA4 + Google Tag Manager (marketing/web), Mixpanel or Amplitude (product analytics and funnel tracking)

CDP: Segment (useful when managing events across multiple tools and teams)

Experimentation: Optimizely, VWO, or AB Tasty for web; LaunchDarkly or native feature flags for in-app experimentation

Qualitative research: moderated user testing, surveys, and compliant session replay where rules permit (coordinate with your Data Protection Officer / DPO)

KYC funnel context: if working with vendors like Veriff, Sumsub, or Onfido/Entrust, ensure event-level data from their SDKs flows into your analytics stack

Key recommendation: Even if you outsource CRO execution entirely, your internal team should own the data contract—what gets tracked, how it’s governed, and how experiment results are stored and shared.

Decision Framework: Should You Hire a Fintech CRO Agency or Build In-House?

Use this scorecard to evaluate which model fits your stage. These thresholds are directional—they’re meant to guide a decision, not replace judgment.

Criterion | Agency | Hybrid | In-House |

Monthly funnel conversions per step | < 500 | 500–2,000 | 2,000+ |

Time to first results needed | < 90 days | 90–180 days | 6–12+ months acceptable |

Engineering capacity for test builds | Low | Partial | Dedicated |

Compliance review turnaround | Slow / undefined | Partial workflow | Defined and fast |

Existing CRO expertise on team | None | Some | Strong |

Budget predictability preference | Fixed retainer | Mixed | Headcount |

Decision rules:

If you need results in under 90 days and can’t hire quickly → start with a conversion rate optimization agency.

If you have high funnel volume, a stable roadmap, and dedicated engineering → build in-house.

If compliance is heavy, volumes are growing, and you need both speed and continuity → choose a hybrid model.

The Hybrid Model: What “Works Better” for Most Fintechs

For most growth-stage fintechs, the strongest setup is hybrid: in-house ownership of strategy, KPIs, and analytics—paired with agency execution of research, design variants, and experimentation support.

Here’s how responsibilities usually split:

In-house owns:

CRO strategy and quarterly OKRs

Analytics instrumentation and data governance

Experiment prioritization and roadmap ownership

Compliance and legal alignment

Agency owns:

Research execution (user testing, funnel analysis, qualitative synthesis)

Design variants and test plans

QA and experiment monitoring

Reporting cadence and learnings documentation

Shared:

Weekly experiment backlog review

Hypothesis scoring and prioritization

Post-test learning sessions

Suggested engagement structure: an 8–12 week discovery/audit sprint to establish baselines, followed by an ongoing retainer focused on experimentation cycles. Re-evaluate the model fit at six months.

How to Choose a CRO Agency for Fintech

Not all CRO agencies understand regulated funnels. Use this checklist before engaging one.

Checklist:

Experience with fintech onboarding—specifically KYC/KYB flows and trust signals

A clear methodology for working inside compliance and legal review cycles

Transparent experimentation process (hypothesis → build → measure → document)

A defined implementation plan: who builds the tests, and how?

Security posture for third-party scripts in authenticated environments

Reporting that includes a learnings repository—not just per-test slide decks

Red flags:

Guaranteed conversion uplift promises (credible practitioners don’t offer these)

No plan for instrumentation or baseline measurement

No experience collaborating with legal/compliance stakeholders

Reporting that shows results but doesn’t capture transferable learnings

WSA’s portfolio of digital finance projects is a useful reference for the kind of work and methodology to look for when evaluating agency experience.

How to Build an In-House CRO Function (Without Wasting 6 Months)

The biggest mistake fintechs make when building in-house is hiring the wrong first role—or hiring before the infrastructure to support experimentation exists.

A realistic 90-day build path:

Days 1–30: Foundation

Hire a Growth PM or CRO Lead (prioritize analytical and cross-functional ability over pure design)

Audit tracking and identify broken events or missing funnel steps

Map the compliance review workflow for copy and UI changes

Days 31–60: Infrastructure

Implement or validate your experimentation platform

Create a shared hypothesis log and a test documentation template

Run your first low-risk, high-impact tests: landing page clarity, onboarding error states, form field labeling

Days 61–90: Cadence

Establish a bi-weekly experiment review cycle

Document learnings—even from tests that don’t win

Define CRO KPIs: KYC completion rate, funding rate, time-to-verified, first transaction rate

Common Mistakes When Deciding Agency vs In-House in Fintech

Treating CRO as a set of A/B tests instead of a continuous learning program

Running tests without clean baseline tracking (results become meaningless)

Optimizing only the top of funnel (signup) while ignoring KYC and funding drop-off—where the revenue impact usually sits

Letting compliance become a permanent blocker instead of building a repeatable review workflow

Not maintaining a learnings repository (tests get forgotten and mistakes repeat)

Hiring a solo “CRO manager” and expecting full-funnel results without analytical and engineering support

Next Steps: A Practical Way to Start (Even If You’re Unsure)

Before committing to either model, a CRO readiness assessment is often the most useful first step. It reviews four areas: tracking coverage, funnel drop-off points, UX friction in KYC and funding flows, and compliance constraints on experimentation.

The output is a clear picture of where conversion is leaking, what’s blocking tests from shipping, and which operating model is most likely to generate results within your current constraints.

WSA works with fintech teams on exactly this: establishing baselines, identifying the highest-impact funnel improvements, and building a sustainable experimentation approach that works inside regulated environments.

Ready to find out where your fintech funnel is leaking?

Get a structured CRO readiness review with a team that understands regulated onboarding, KYC friction, and experimentation governance.

Book a discovery call →

FAQ

Is it better to outsource CRO for a fintech?

When you need faster time-to-value, specialist skills, or don’t have the bandwidth to hire a full team, outsourcing CRO is often the fastest way to start generating actionable learnings. For most seed-to-Series B fintechs, starting with an agency—while building internal data ownership—is typically the lower-risk path.

How much does a fintech CRO agency typically cost?

CRO agency pricing typically ranges from $8,000–$25,000/month on retainer, depending on scope. A standalone audit and roadmap usually costs $15,000–$40,000. Costs rise with implementation support, research depth, and experimentation volume. Always confirm whether the retainer includes test builds or only strategy and design.

What roles do you need for an in-house CRO team?

A minimum viable in-house CRO team includes a CRO Lead or Growth PM, an analyst, a UX designer, and engineering support. A single “CRO manager” without analytical and implementation resources usually can’t move fast enough to justify the role. In fintech, consistent access to a compliance stakeholder is also non-negotiable.

What metrics matter most for fintech CRO (beyond signup conversion)?

The highest-value metrics are KYC/KYB completion rate, funding/deposit completion rate, time-to-verified, first transaction rate, and 30-day activation. This is where revenue is typically won or lost—not at the top-of-funnel signup step.

Can fintechs run A/B tests with compliance restrictions?

Yes—but A/B testing in regulated industries requires governance: pre-approved claim libraries, review workflows for changes touching financial terms, and documented experimentation guardrails. With the right process, compliance becomes a checkpoint—not a bottleneck.

When should a fintech switch from an agency to in-house?

When conversion work is continuous (not project-based), funnel volumes are high enough to support statistically valid tests each month, and the organization can dedicate at least a CRO lead, an analyst, and engineering capacity to the experimentation program—that’s a strong signal to internalize the function.

Does CRO mean conversion rate optimization or Chief Risk Officer in fintech?

Both terms use the “CRO” abbreviation in financial services. This article focuses entirely on conversion rate optimization—improving funnel completion rates through research, testing, and iteration. The Chief Risk Officer is a separate executive role.

Launch Your Licensed Brokerage with Confidence

We support brokers and fintechs through licensing, launch planning, and everything a regulated brand needs to go live.