•

•

How to Launch a Fintech Company in 2026: Step-by-Step Guide for Founders

If you're going to launch a fintech company in 2026, you need regulatory clarity, secure infrastructure, capital planning, compliance architecture, banking relationships, and an operational and compliant website before you even go public.

Founders often launch their product first and consider the legal pages and compliance documents as things to worry about "later." This has consistently resulted in 3-9 month delays, banking rejections, and failed licensing attempts.

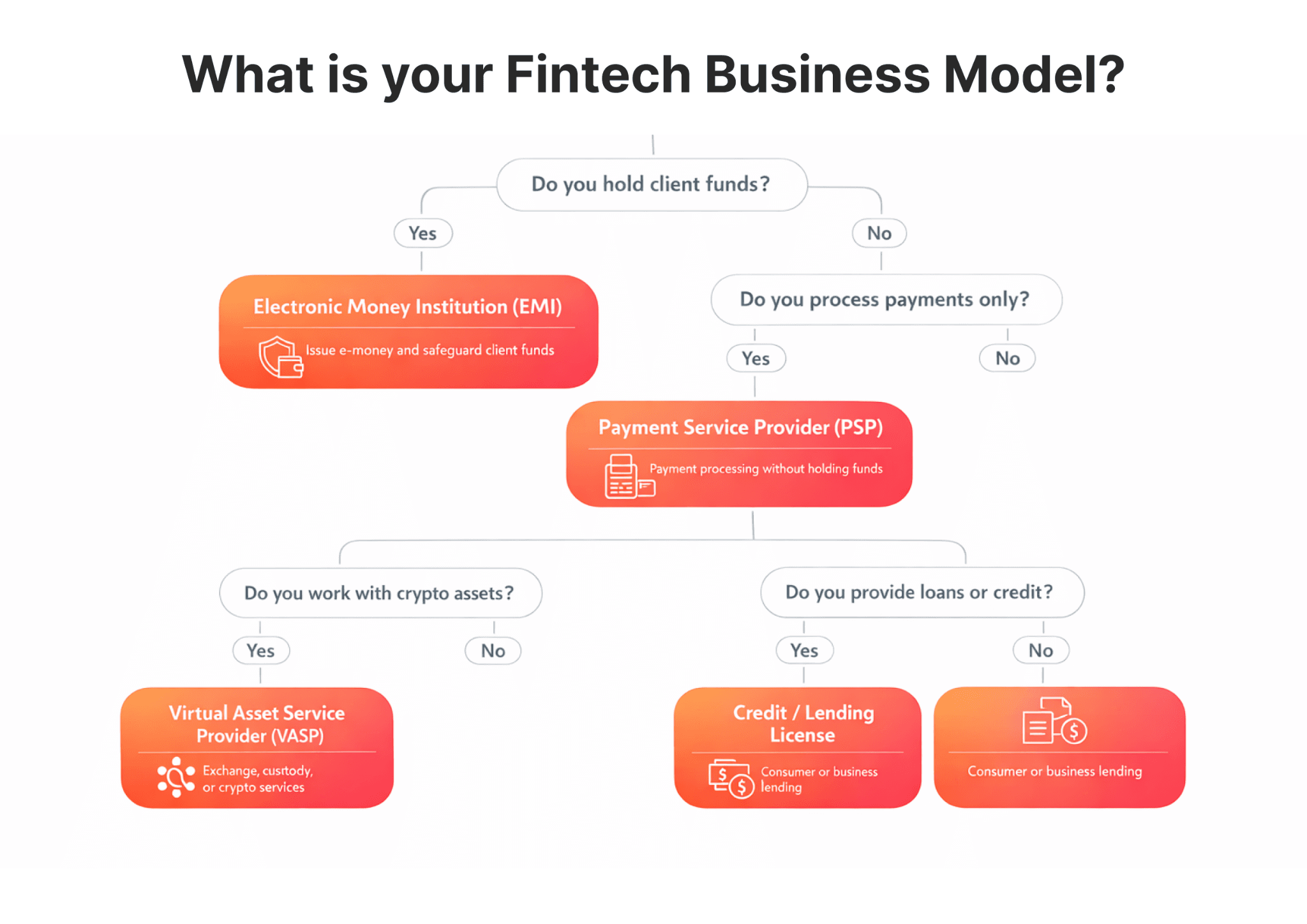

Step 1: Define Your Fintech Business Model and Regulatory Category

Before you even begin the process of obtaining a license or writing the first line of code, you need to determine what kind of fintech company you are. This is important because it determines your capital requirements, the type of license you need, the AML/KYC requirements, and your overall regulatory obligations.

The main regulatory categories include:

Digital banking / Electronic Money Institution (EMI) — licensed to issue electronic money and hold customer funds

Payment Service Provider (PSP) — processes payments without holding e-money

Crypto Exchange or Custody Provider (VASP) — exchanges or holds digital currencies under the emerging regulatory framework for VASPs

Brokerage or Trading Platform — executes trades of securities, FX, or CFDs on behalf of customers

Lending platform — provides consumer or business credit

Embedded finance/BaaS provider — provides a platform to integrate financial services into a non-financial product

Each of these categories has its own capital requirements, reporting obligations, and geographical constraints. Failure to understand your regulatory category can render your application invalid, cause a six-month delay or longer in the licensing process, and force a complete restructuring of your business entity.

Example: Revolut initially launched as a prepaid card business, which eventually led to the company’s UK Electronic Money Institution license in 2018. Revolut’s regulatory structure was designed to align with the company’s product at the time.

Step 2: Understand the Fintech Licensing Process in Your Target Jurisdiction

Plan for 6–18 months from application to approval. The wrong jurisdiction choice can limit your banking access, target market, and scalability.

Jurisdiction | Regulator | Timeline | Min. Capital (EMI) |

|---|---|---|---|

United Kingdom | 6–12 months | £350,000 | |

EU (Cyprus) | 6–12 months | €350,000 | |

Australia | 6–12 months | AUD 1,000,000+ | |

Singapore | 9–18 months | SGD 1,000,000 | |

Switzerland | FINMA | 9–18 months | CHF 10,000,000 |

Offshore | FSA/FSC | 3–6 months | $50,000–$100,000 |

[aa fast fact]

What most founders don't expect: Regulators frequently review your website during the licensing process. Missing legal pages or absent risk disclosures can pause or reject your application.

[/aa]

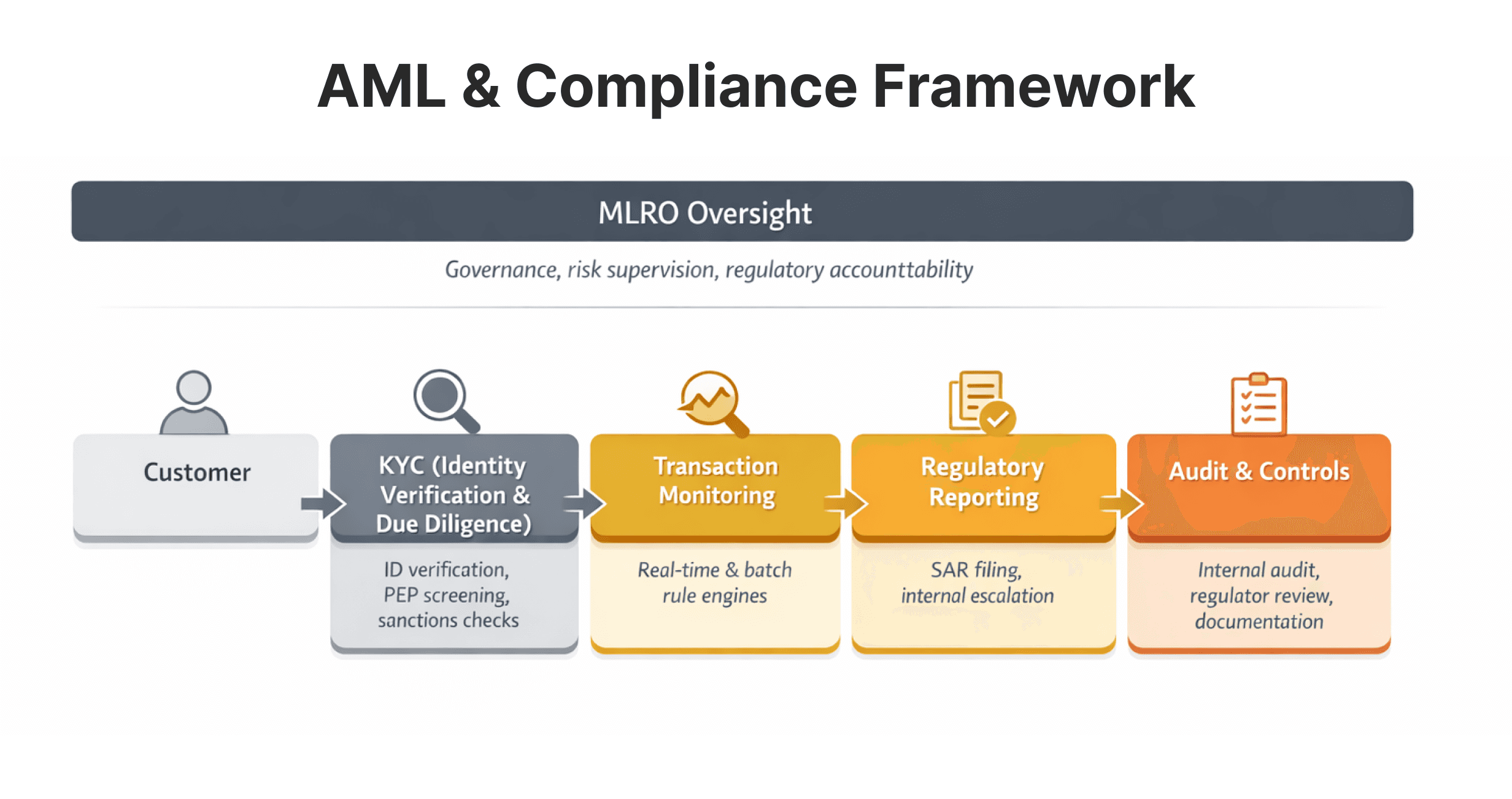

Step 3: Build Your Compliance and Risk Framework from Day One

Compliance is operational infrastructure — not a post-launch checklist. Retrofitting the AML program and the KYC process into the existing stack takes 3 to 9 months, and in many cases, this involves breaking changes to the product.

Day-One Requirements:

AML/KYC policy: customer due diligence, PEP checks, sanctions screening

Transaction monitoring: real-time and batch rule sets for suspicious activity transactions

GDPR and data protection: data retention policies, DPA agreements, consent management

Internal controls: segregation of duties, audit trails, access management

Risk disclosures: risk warnings specific to the product, e.g., investor, trader, or borrower risk warnings

Third-party audits: independent AML and IT security audits

AML vendors like Comply Advantage, Sumsub, and Sardine provide modular tools that integrate with most fintech stacks. Engaging one early — before your product is built — saves significant rework.

Appointing a qualified MLRO is mandatory in most jurisdictions before license approval. In the FCA's 2023 review, incomplete AML frameworks were the most frequent reason for application rejection.

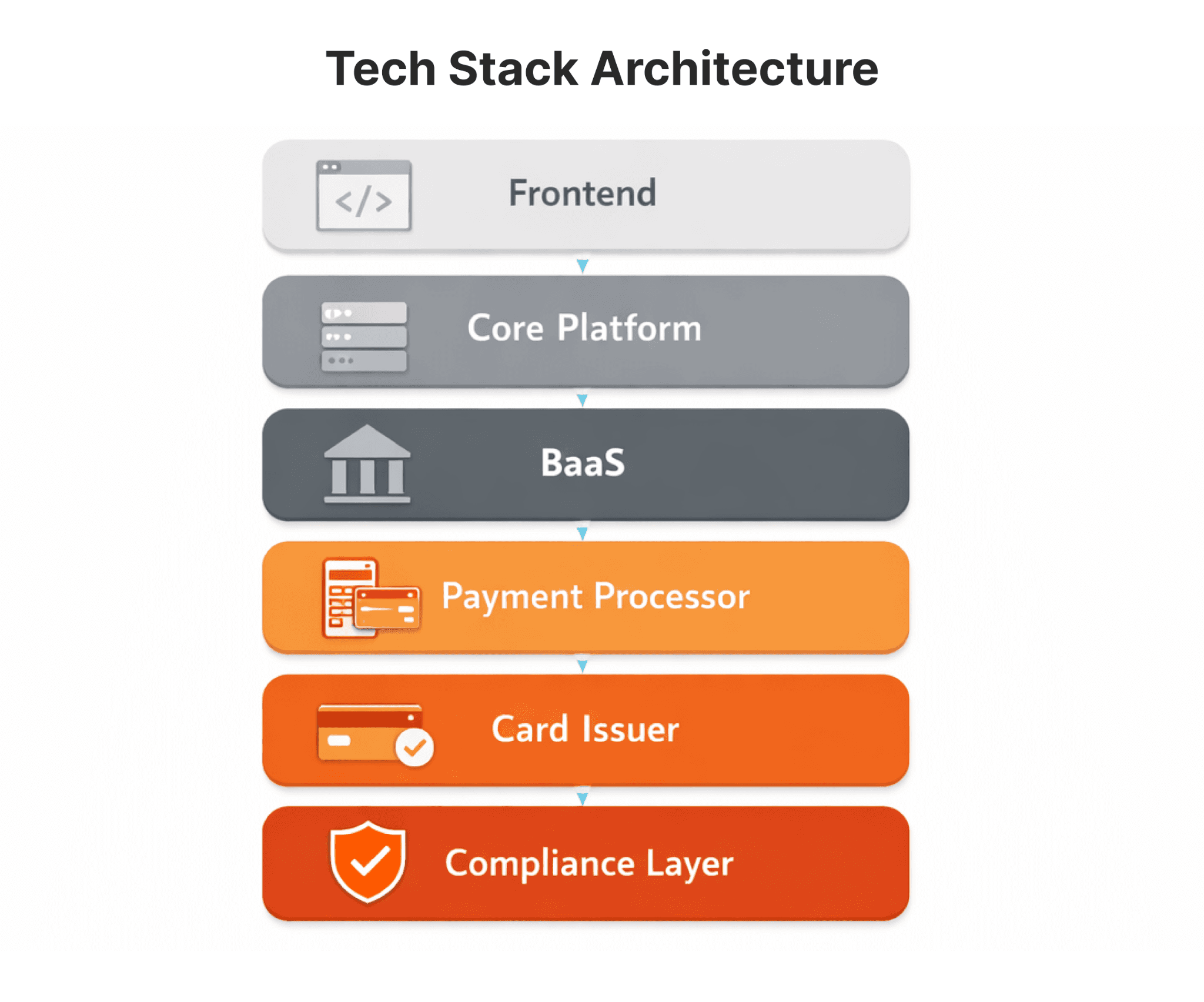

Step 4: Design Your Technology and Infrastructure Stack

Most early-stage founders should default to white-label or API-modular infrastructure. Custom builds extend timelines and create compliance exposure.

Approach | Time to Market | Best For |

|---|---|---|

White-label | 4–8 weeks | MVP, licensing phase |

API-modular | 8–20 weeks | Series A onwards |

Custom build | 6–18 months | Post-PMF, scaled products |

Core infrastructure layers: BaaS providers (Solaris, Railsr), payment processors (Stripe, Adyen), card issuers (Marqeta), crypto custodians (Fireblocks, BitGo).

Step 5: Develop and Launch a Compliance-Ready Fintech Website in Parallel

A fintech website is a regulatory, banking, and investor-facing asset. It must be developed during the licensing process, not after approval.

Your website is reviewed at multiple critical moments: by regulators during licensing, by banking partners before account opening, by investors during due diligence.

A compliant fintech website must include:

Clear product description with no misleading claims

Transparent fees and risk information

Legal pages: Terms & Conditions, Privacy Policy, Cookie Policy, AML Statement

Licensing information, SSL certificate, Core Web Vitals optimization

Analytics (GA4, GTM) and investor trust signals

Step 6: Prepare Your Go-To-Market Strategy

Global fintech funding for 2023: $113.7 billion (KPMG Pulse of Fintech, H2 2023). The distinction between a funded and an unfunded startup is now largely a matter of clarity on “go-to-market.”

The main GTM areas: customer groups, competing on compliance/user experience/price against incumbents; paid acquisition via Google Ads + LinkedIn; SEO + GEO on high intent fintech startup search volume; partnerships via BaaS; PR via regulatory-forward PR releases; affiliate/IB; CAC vs LTV modeling pre-launch of any paid acquisition strategy.

Before scaling marketing, ensure you have checked off compliance and website readiness. Running paid marketing before your legal pages and risk disclosures are live is a regulatory risk and a budget drain on traffic you can't legally acquire.

Step 7: Secure Banking, Liquidity, and Strategic Partnerships

Banking relationships are the most fragile and underestimated element of a fintech launch. Many companies build strong products, secure licenses, and still fail here due to inadequate documentation, unresolved AML findings, or a website that doesn't clearly explain the business model to a bank's compliance team.

Build these relationships 6–12 months before intended launch — banking partner onboarding routinely takes 2–4 months independently of your licensing process.

Key relationships to establish: safeguarding accounts (a requirement for EMIs and PSPs to ring fence customer funds), correspondent banking to facilitate cross-border payments, liquidity providers (prime brokers, crypto OTC desks, FX aggregators), payment gateways (Stripe, Adyen, Checkout.com), fintech specialist legal advice, and external compliance consultants to assist in pre-submission checks.

Step 8: Conduct Pre-Launch Testing and Regulatory Readiness Review

Every item must be complete before your first public marketing campaign:

Legal review of all website content, AML/KYC workflow testing, security penetration testing, transaction flow testing, GDPR audit, load testing, and final website sign-off by compliance officer and legal counsel.

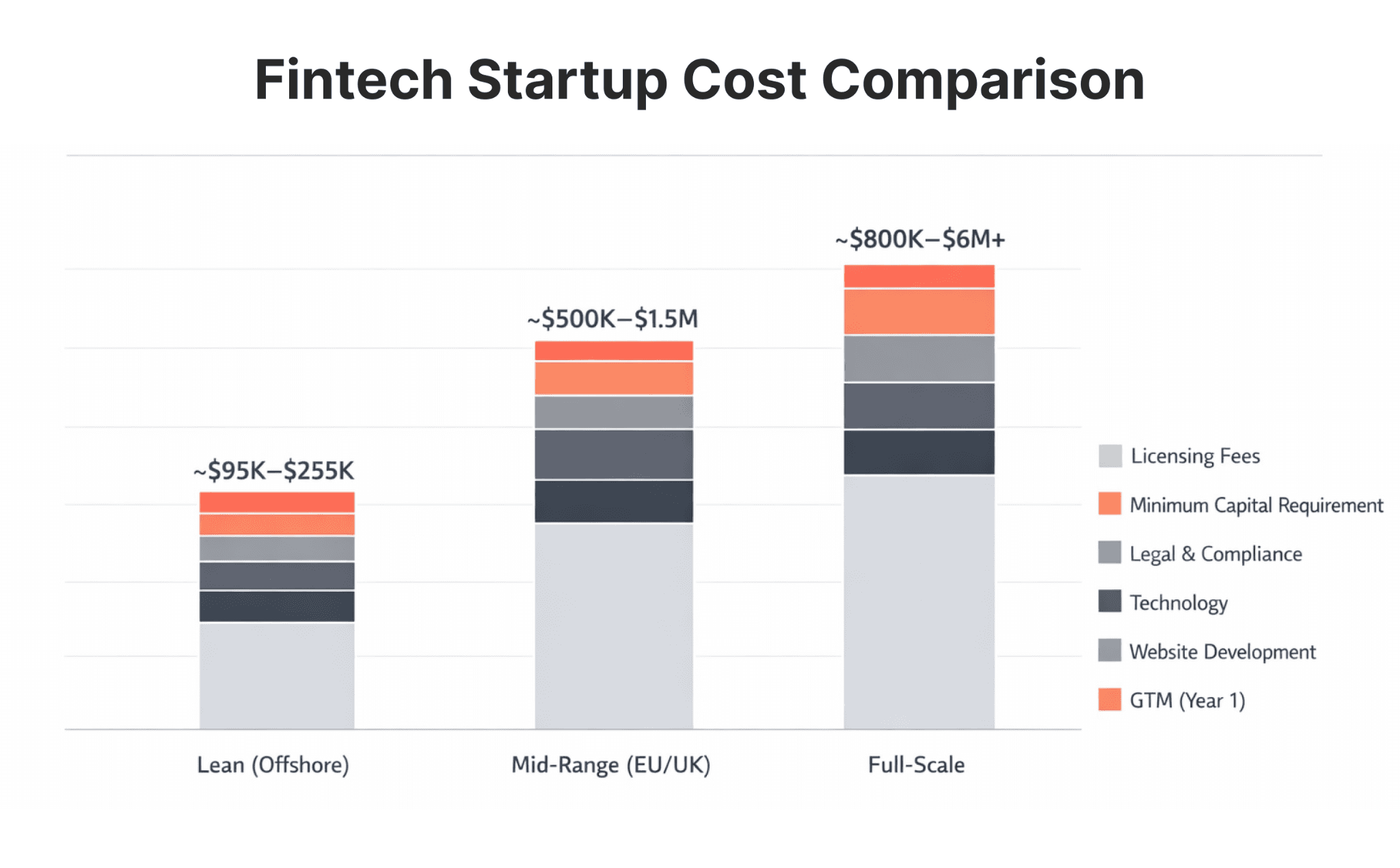

Fintech Startup Cost Breakdown

Cost Category | Lean | Mid-Range (EU/UK) | Full-Scale |

|---|---|---|---|

Licensing fees | $5K–$20K | $20K–$80K | $80K–$300K |

Min. capital requirement | $50K–$100K | €350K–€1M | £350K–£5M+ |

Legal & compliance | $15K–$40K | $40K–$120K | $100K–$400K |

Technology | $10K–$50K | $50K–$200K | $200K–$600K |

$5K–$15K | $10K–$40K | $20K–$80K | |

GTM (Year 1) | $10K–$30K | $30K–$100K | $100K–$500K |

Total | ~$95K–$255K | ~$500K–$1.5M | ~$800K–$6M+ |

Common Mistakes When Launching a Fintech Company

Underestimating the time required for obtaining licenses. The founders estimate 3-4 months, while the process takes 6-18 months.

Selecting the jurisdiction based on costs. Offshore licenses can restrict access to banking and markets.

Not having a qualified Compliance Officer. Regulators require the nomination of an MLRO before issuing licenses.

Not starting the website development before the licenses are obtained. This process can delay the regulatory process, banking, and investors.

Weak website trust signals. Missing team pages, no regulatory references, and absent risk disclosures undermine investor confidence.

No analytics infrastructure. Launching without GA4 and GTM means no performance baseline.

Overbuilding custom technology too early. Default to white-label until product-market fit is established.

Ignoring investor due diligence requirements. Gaps in licensing status or website legal completeness delay or kill funding rounds.

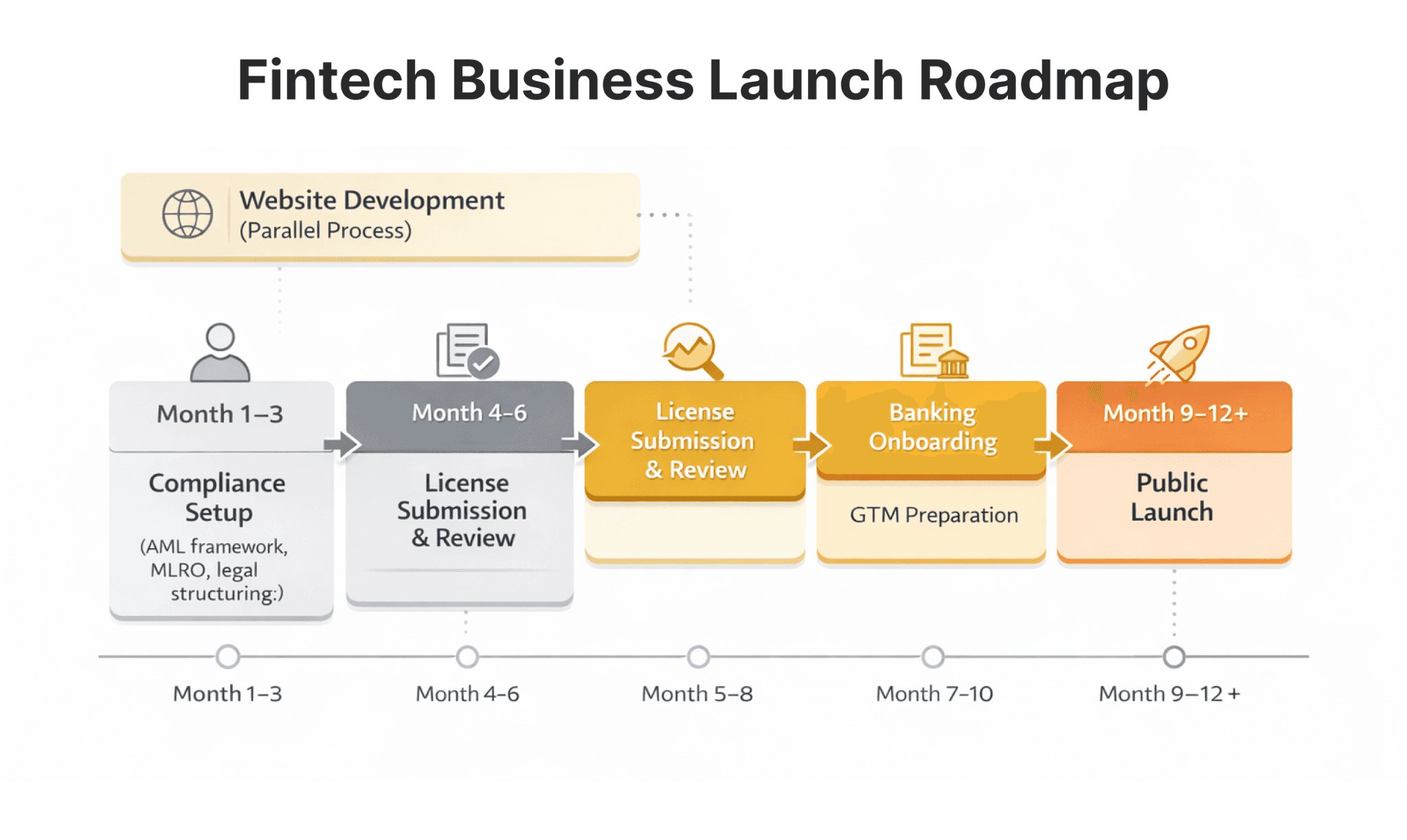

Structured Launch Roadmap

Phase | Timeline | Key Actions |

|---|---|---|

Foundation | Months 1–2 | Define business model, jurisdiction, regulatory category |

Compliance setup | Months 2–4 | AML framework, compliance officer, legal counsel |

Infrastructure + Website | Months 3–6 | Tech stack, compliance-ready website build (parallel to licensing) |

License submission | Month 6 | Website must be live or in final review |

Banking onboarding | Months 6–10 | Safeguarding accounts, liquidity |

GTM preparation | Months 8–11 | Positioning, SEO, partnerships |

Pre-launch review | Months 11–12 | Penetration testing, compliance audit, website sign-off |

Public launch | Month 12+ | Regulatory approval confirmed |

FAQs

How long does it take to launch a fintech company?

The launch of most fintech companies takes 6-18 months. FCA and MAS licenses are on the longer side. Offshore licenses are faster but come with compromises.

What are the fintech licensing requirements? The basic requirements include the following:

Business plan

AML/KYC Policy Manual

MLRO

Audited financials

IT Security Assessment

Operational website with full legal pages

What are the fintech licensing requirements?

Core requirements: detailed business plan, AML/KYC policy manual, named MLRO, audited financials, IT security assessment, and a fully operational website with complete legal pages.

How much does it cost to start a fintech startup?

From ~$95,000 for a lean offshore MVP to $6M+ for a fully licensed platform in a major jurisdiction. The largest variables are minimum capital requirements, legal and compliance advisory, and technology.

Do I need a compliance officer before launch?

Yes — a named MLRO is required before license approval in most jurisdictions. They must meet the regulator's fit-and-proper criteria and be formally named in the application.

When should I build my fintech website?

During the licensing process — not after approval. Regulators, banking partners, and investors all review it before you launch. A website lacking required legal content independently delays each of these critical relationships.

Whether you’re launching something new or improving an existing platform, we’re ready to discuss your goals and explore the best way forward.