•

•

Fintech MVP Development: What to Launch First (and What to Skip)

Most fintech products don’t fail because teams ship too little. They fail because teams ship too much of the wrong things—or ship something technically impressive that still can’t safely handle money, pass a partner compliance review, or earn enough user trust to convert.

Fintech MVP development is different from building a SaaS tool or consumer app. “Viable” in financial products doesn’t just mean functional—it means trustworthy, auditable, and responsible enough to run a real pilot with real money. At the same time, overscoping a fintech MVP is one of the fastest ways to burn runway before you’ve validated anything.

This guide gives you a practical sequencing framework. By the time you finish reading, you should be able to sketch your first-release scope in under an hour—knowing exactly what to include, what to defer, and why.

Key Takeaways

A fintech MVP must complete one full “money loop,” not a collection of partial features.

KYC, security, and operational controls aren’t Phase 2 items—they’re part of what makes the product viable.

Pick one geography, one payment rail, and one primary use case for v1. Everything else is a complexity multiplier.

Skip multi-currency, rewards, AI insights, and advanced dashboards until you’ve validated activation and retention.

Use vendors for regulated infrastructure early (KYC/IDV, rails, fraud). Build your differentiators later.

“Launch fast” doesn’t mean “launch without controls.” It means shipping the minimum that’s safe, functional, and testable.

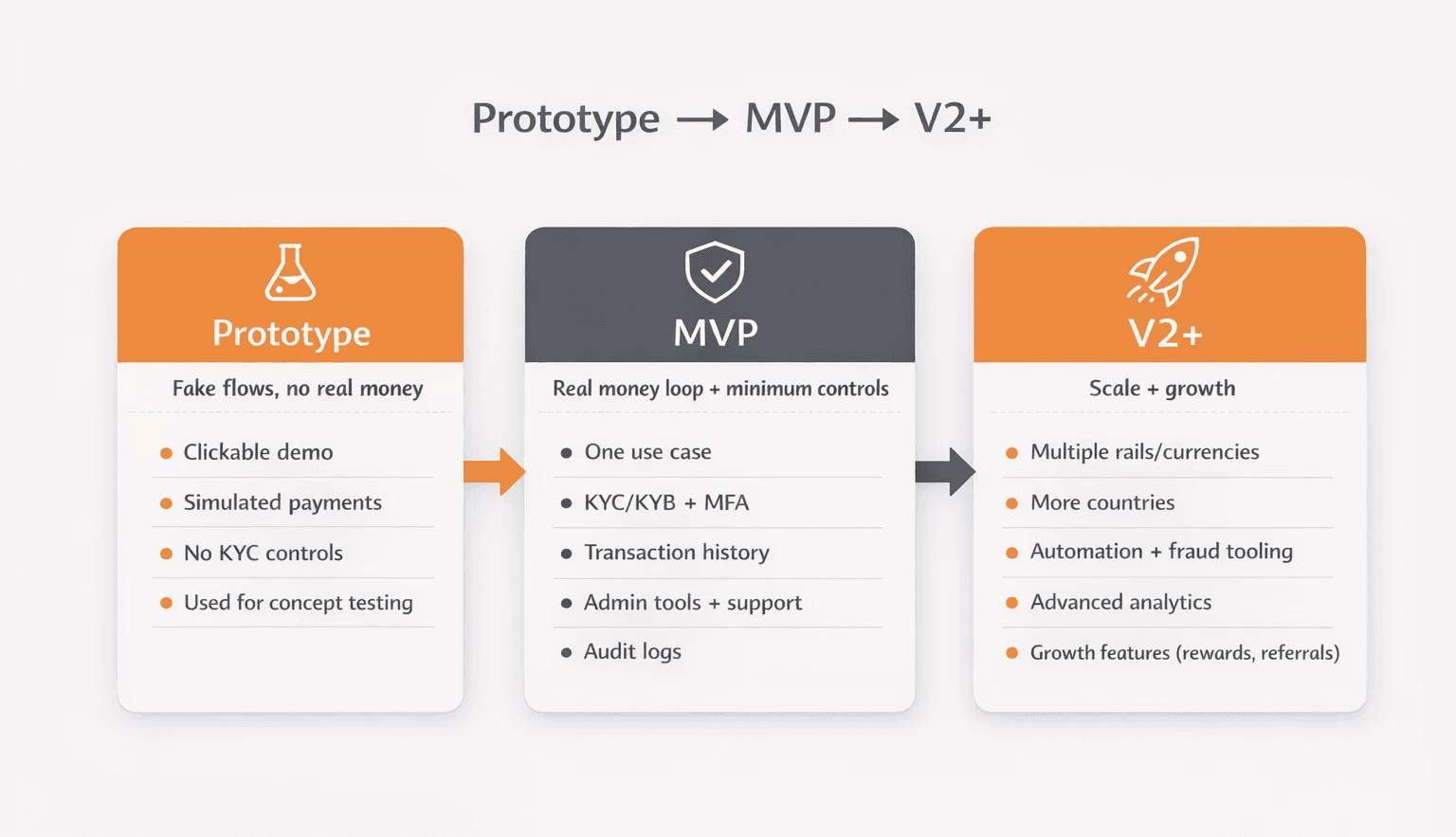

What Counts as an MVP in Fintech (and What Doesn’t)?

A fintech MVP is a working product that safely delivers one core financial outcome for a specific, narrow audience—with the baseline trust and auditability that financial services require.

It’s not a prototype with placeholder flows. It’s not a demo where the “payment” is simulated. And it’s not a near-finished product waiting on one missing feature. An MVP is the smallest real, working version that lets you test whether the core value proposition holds up with actual users handling actual money.

The most common mistake teams make is treating compliance infrastructure and operational tooling as “Phase 2.” They aren’t. In a financial product, a user who gets stuck during identity verification, can’t contact support after a failed transfer, or has no way to dispute a transaction doesn’t have a bad experience—they have a broken product. You can simplify scope significantly in a fintech MVP, but you can’t simplify responsibility.

Step 1 — What Exact User Outcome Are You Validating First?

Before you scope a single feature, define the one job your product needs to do—end to end—for v1. Everything else is a distraction until this job works.

This is the “one job to be done” rule. Each fintech model has a natural starting point:

Wallet / payments: “A user can send money to one person or pay one merchant type.”

Lending: “A user applies, receives a decision, and gets funds disbursed for one product type.”

Wealth / investing: “A user onboards, funds their account, and executes one buy or recurring investment action.”

B2B spend / expense: “A user creates a sub-account, issues a virtual card, sees a transaction, and exports a report.”

Your fintech MVP roadmap should be reverse-engineered from this outcome. If a feature doesn’t help a real user complete this job reliably and safely, it belongs in the backlog.

Step 2 — Map the “Money Loop” (the Minimum End-to-End Flow)

The money loop is the complete, unbroken path from first contact to a completed financial action and its confirmation. If any step in the loop breaks, you don’t have an MVP—you have a demo.

Map your loop across these seven stages:

Entry — landing page, invite, or referral

Account creation — registration, consent capture

Identity / verification — KYC/KYB, risk screening

Funding / authorisation — connecting a bank, topping up, or issuing credit

Core transaction or action — the actual money event

Confirmation + history — receipt, status, transaction list

Support + recovery — what happens when any of the above fails

Test this loop manually with real users before calling anything “done.” Most launch delays come from breaks discovered in step 6 or 7—the parts that are easiest to defer and the most damaging to trust when they fail.

Step 3 — What to Launch First: The Non-Negotiable MVP Feature Stack

The minimum viable feature set for a fintech product covers seven functional blocks. Each one is required. None of them is optional for a real-money pilot.

Block A: Identity + Onboarding

A sign-up flow, clear consent capture and privacy disclosures, and a KYC or KYB flow appropriate to your product and jurisdiction. This can include a manual review step behind the scenes—automated decisioning isn’t required for v1. Vendors such as Veriff, Sumsub, and Onfido (Entrust) offer integrations that can significantly reduce build time. Consult qualified compliance and legal counsel to confirm the verification standard required for your product and jurisdiction.

Block B: Secure Access

Multi-factor authentication (MFA/2FA), session management, account lockouts after repeated failed attempts, and a working password-reset flow. These aren’t “nice to have”—they’re the baseline expectation for any product handling financial accounts.

Block C: The Core Money Feature

One primary action, end to end: transfer, payment, investment, loan disbursement, or card transaction. Not a demo of that action—the real thing, with real settlement and real movement of funds.

Block D: Minimum Ledgering + Transaction History

A transaction list with statuses and receipts, plus consistent balance logic. The UI doesn’t need to be sophisticated, but it must be accurate. Users who can’t verify what happened to their money don’t come back.

Block E: Operational Tooling

An internal admin console—even a basic one—that allows your team to: look up users, review flagged transactions, manually approve or decline edge cases, disable accounts, and replay failed webhooks or notifications. This is the most commonly underscoped block in early fintech product development. Without it, your team can’t operate the product safely.

Block F: Support + Trust

A contact channel with clear response expectations, a basic dispute or complaint intake process, and in-app messaging for common failure states (“Your transfer is under review—we’ll notify you within 24 hours”). Users of regulated financial products expect to reach someone when something goes wrong.

Block G: Analytics + AuditabilityEvent tracking for every key funnel step (account creation, KYC start/completion, funding, first transaction), plus audit logs for sensitive administrative actions. Both are needed from day one: analytics to measure what’s working, logs to support compliance and partner reviews.

Launch First vs. Later: Feature Reference Matrix

Feature / Capability | Launch First | Defer to V2+ |

|---|---|---|

KYC/KYB identity verification | ✅ | — |

MFA / secure session management | ✅ | — |

Core money action (one rail, one use case) | ✅ | — |

Transaction history + balance | ✅ | — |

Admin console (basic) | ✅ | — |

Support channel + dispute intake | ✅ | — |

Audit logs + event tracking | ✅ | — |

Multi-currency / multi-rail support | — | ✅ |

Rewards, points, referral programme | — | ✅ |

Advanced analytics dashboards | — | ✅ |

Multiple user roles / permission levels | — | ✅ |

AI-driven insights or recommendations | — | ✅ |

Multi-country launch | — | ✅ |

Social / community features | — | ✅ |

Step 4 — What to Skip in a Fintech MVP (Scope Killers That Don’t Validate the Core)

Skip product breadth. Never skip safety. The features below routinely consume 30–60% of MVP build time while doing little to validate your core value proposition.

1. UX Polish That Doesn’t Affect Conversion or Trust

Complex design systems, animation-heavy interfaces, deep personalisation, multiple brand themes, and micro-interaction tweaks. Ship functional and clear. Make it beautiful in v2.

2. Complexity Multipliers

These are the scope killers that turn a 10-week build into a 9-month build:

Multi-country launch — regulatory complexity multiplies with every jurisdiction

Multi-currency — FX handling, display logic, and ledgering complexity are significant

Multiple payment rails — each rail has its own integration, testing, and failure modes

Multiple user roles / permissions — fine-grained access control is complex; start with one role

Multi-entity or multi-tenant accounting — adds legal and ledgering complexity that’s hard to retrofit later. If your core model requires it, plan for it early.

3. Monetisation and Growth Features Before Activation Is Proven

Rewards and points programmes, referral mechanics, subscription tiers with complex billing logic, “AI insights,” push notification campaigns, and social features. These are growth levers—they have little value until the core product works and retains users.

⚠️ Important: This section is about skipping optional product breadth. Do not skip security controls, identity verification, audit logging, or operational tooling. Those aren’t “extra”—they’re what makes the product viable in a regulated context.

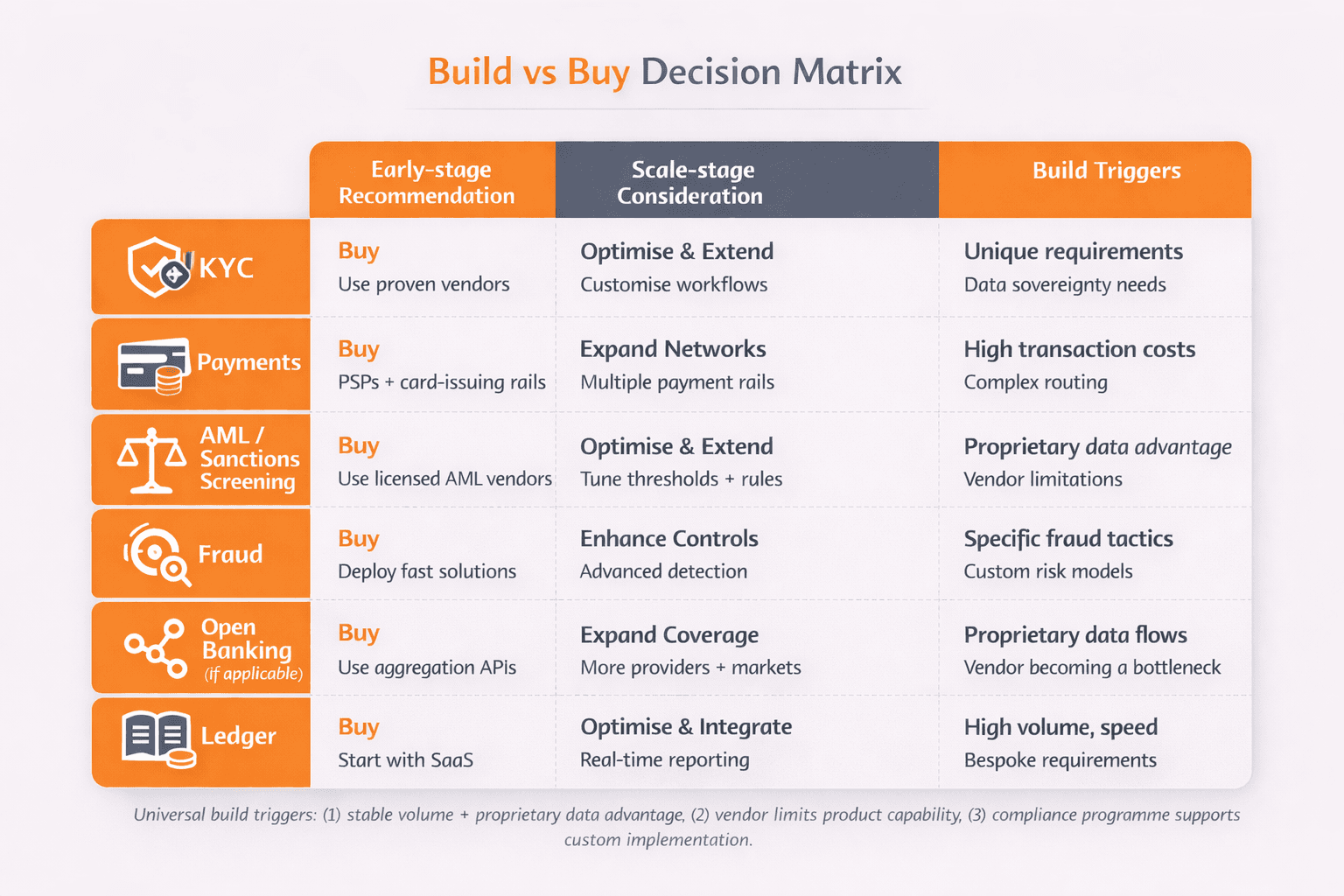

Step 5 — Build vs. Buy: Which Integrations to Add Early (and Which to Delay)

In early fintech product development, the default position should be: buy the regulated infrastructure, build the differentiated experience.

Use vendors for:

KYC/IDV and KYB verification

Sanctions screening and AML transaction monitoring (at appropriate thresholds—consult legal counsel)

Payment processing (PSPs) and card-issuing rails

Fraud scoring (rule-based or third-party)

Open banking aggregation (if applicable)

Build in-house when:

You have stable transaction volume and a clear data advantage from a proprietary approach

The vendor’s capability has become your product’s limiting factor

You have the compliance programme to support a custom implementation

When evaluating vendors for your fintech MVP, assess: geographic coverage and licensing, pricing at low volume, time-to-integrate, compliance posture and data residency, audit and reporting support, reliability SLAs, and the quality of developer documentation.

Step 6 — Compliance and Security You Can’t Skip (Even in MVP Mode)

“MVP mode” doesn’t suspend compliance obligations or security expectations. It means doing the minimum that’s safe and legal—not less than that.

This is not legal advice. For your product, jurisdiction, and partner requirements, consult qualified compliance and legal counsel. That said, here are baseline controls every fintech app MVP should have in place before a real-money pilot:

Baseline controls checklist:

KYC/KYB verification flow appropriate to product and jurisdiction

Sanctions screening at account creation (and ongoing where required)

AML considerations defined—at minimum, a documented approach appropriate to your risk level

Privacy policy and terms of service reviewed by legal counsel

Data encrypted at rest and in transit

MFA / strong authentication for users and all admin access

Audit logs for sensitive actions (account creation, fund movements, admin changes)

Least-privilege admin access (no broad database access for all team members)

Basic incident response process—who gets called when something breaks at 2am

If handling card data: understand your PCI DSS obligations before going live

AML compliance for fintech and KYC requirements vary significantly by jurisdiction, product type, and whether you operate under your own licence or a partner programme. Don’t assume what applied to another fintech applies to yours.

Step 7 — MVP Architecture That Keeps You Fast Now and Flexible Later

Start with a modular monolith. Premature microservices are one of the most common architecture mistakes in early fintech product development—they add operational complexity before you have the team or volume to justify it.

Practical patterns that work well for fintech MVPs:

Single codebase with modular domains — separate concerns (identity, ledger, payments, notifications) within one deployable unit; refactor into services once you have clear boundaries and owners

Adapter/gateway layer for vendor integrations — wrap every third-party service (KYC vendor, PSP, fraud tool) behind internal interfaces so you can switch providers without rewriting core logic

Event logging from day one — log key financial events immutably; this is both an audit trail and the foundation of future reporting and analytics

Feature flags — enable controlled rollouts to subsets of users; critical for managing risk during early fintech MVP testing

Clean separation between core logic and payment rails — your business rules shouldn’t be entangled with a specific provider’s API

Step 8 — MVP Success Metrics: What to Measure From Day One

Define success metrics before launch, not after. The goal is to learn—and you can only learn if you know what you’re measuring.

Funnel metrics (instrument from day one):

Onboarding start → KYC submission rate

KYC submission → verification completion rate and average time-to-verify

Verified → funding / deposit completion rate

Funded → first transaction rate (activation)

First transaction → second transaction (early retention)

Operational health signals:

Transaction failure rates and error breakdown by type

Fraud flags and chargeback rates

Support ticket volume by category

Admin intervention rate (manual reviews as % of total)

North star metric examples by model:

Payments: weekly active senders

Lending: applications that reach a funded state within X days

Wealth: funded accounts with at least one completed investment

B2B: cards issued with at least one transaction in the first 30 days

Need a fintech website that loads fast, builds trust, and converts?

WSA designs and develops fintech sites with performance, clarity, and compliance-ready structure in mind.

Pre-Launch Checklist for a Fintech MVP

Before your first real-money pilot, verify each of the following:

End-to-end money loop tested: happy path and all critical failure states

KYC/KYB flow tested with edge cases (manual review process defined and staffed)

Error states produce clear, honest user messaging

Monitoring, alerting, and error logging are live and tested

Admin console access limited to named individuals; access logging in place

Support channel live with a defined response SLA

Legal pages (privacy policy, terms of service) reviewed and published

Basic incident response process documented and shared with the team

Pilot plan defined: who are the first users, how many, and what does success look like at 30 days?

After Launch: How to Iterate Without Turning Your MVP Into a Monster

The period immediately after an MVP launch is the highest-risk time for scope creep. Every piece of feedback feels urgent. Most of it isn’t.

A practical iteration framework:

Fix funnel drop-offs first. If users fail at KYC, fix that before building new features. Activation and retention gaps outrank new capability every time.

Add one capability at a time. One new payment rail. One new country. One new user segment. Stacking expansions multiplies risk and stretches testing coverage.

Prioritise by impact × effort × risk. Risk is a first-class dimension in fintech—a feature that marginally improves conversion but introduces new fraud vectors or compliance exposure is rarely worth it this early.

Document your learnings. A lightweight experiment log prevents repeated mistakes and gives investors (and future hires) evidence of methodical decision-making.

Next Steps: Planning MVP Delivery (Team, Timeline, and When to Bring In Specialists)

For many teams, a first real-money fintech MVP pilot takes roughly 10–24 weeks from scoping to launch. The factors that push that range upward are almost always: the number of third-party integrations, partner compliance requirements (bank/PSP/card issuer due diligence), regulatory complexity, platform choices, and the team’s experience building regulated products.

What increases cost and timeline:

Multiple payment rails or card-issuing infrastructure

Custom ledgering (vs. using a ledger-as-a-service vendor)

Multi-country launch with different licensing requirements

Advanced fraud tooling built in-house

Complex admin operations workflows

When to bring in specialists:

Compliance counsel: before finalising your KYC/AML approach and terms of service

Security review: before going live with real user data and money movement

Integration specialists: when a critical vendor integration (PSP, card issuer, KYC provider) is new to your team

Getting scoping right before you write the first line of code is the highest-leverage investment you can make in a fintech MVP. An experienced product and delivery team can help validate scope, map integrations, and identify the compliance constraints that shape your architecture—before they become expensive surprises.

FAQ

How long does it take to build a fintech MVP?

Many fintech MVPs take 10–24 weeks from scoping to a real-money pilot. The biggest timeline drivers are the number of third-party integrations (KYC provider, PSP, card issuer), partner compliance questionnaire processes, regulatory requirements in your target market, and how much of the stack you build vs. buy. Teams that use established vendors for rails and verification typically ship faster than those building custom infrastructure from scratch.

How much does a fintech MVP cost?

Fintech MVP cost varies widely—often $80,000–$250,000+ for a first real-money pilot, depending on scope, team composition, and market. Key cost drivers include: custom ledgering, multiple payment rails, card-issuing infrastructure, advanced fraud tooling, and compliance programme setup. Using vendors for regulated infrastructure and limiting v1 to one use case / one market is the most effective way to control cost without compromising viability.

What features should always be included in a fintech MVP?

The non-negotiable stack: KYC/KYB identity verification, secure authentication (MFA), the core money action end to end, transaction history and balance, an internal admin console, a support channel with dispute intake, and event tracking with audit logs. Skip product breadth—don’t skip any of these.

What should you skip in a fintech MVP?

Skip complexity multipliers: multi-currency support, multiple payment rails, multi-country launch, rewards or referral programmes, advanced analytics dashboards, AI-driven features, and multiple user permission levels. None of these validate your core value proposition in v1. All of them significantly increase build time and operational complexity.

Can I launch a fintech MVP without being fully licensed?

This depends on your jurisdiction, product type, and whether you’re operating under your own licence or a sponsor bank / licensed partner programme. Many early-stage fintechs launch under a partner’s regulatory umbrella (embedded finance / BaaS models) while pursuing their own licence in parallel. This is highly jurisdiction-specific—consult qualified compliance and legal counsel before making assumptions about regulatory obligations.

Launch Your Licensed Brokerage with Confidence

We support brokers and fintechs through licensing, launch planning, and everything a regulated brand needs to go live.